IMA CMA Financial Planning Performance and Analytics CMA Part 1: Financial Planning – Performance and Analytics Exam Online Training

IMA CMA Financial Planning Performance and Analytics Online Training

The questions for CMA Financial Planning Performance and Analytics were last updated at Apr 02,2026.

- Exam Code: CMA Financial Planning Performance and Analytics

- Exam Name: CMA Part 1: Financial Planning - Performance and Analytics Exam

- Certification Provider: IMA

- Latest update: Apr 02,2026

Which one of the following best describes the difference between a normal costing system and an actual costing system?

- A . Direct labor cost is estimated using a predetermined rate under a normal costing system, while it is the actual value under an actual costing system.

- B . Direct material cost is estimated using a predetermined rate under a normal costing system while it is the actual value under an actual costing system

- C . Factory overhead cost is estimated using a predetermined rate under a normal costing system,while it is me actual value under an actual costing system.

- D . Both direct labor cost and direct material cost are estimated using a predetermined rate under a normal costing system, while they are the actual value under an actual costing system

Company A currently uses U.S GAAP while Company 8 is currently using IFRS. Both companies are individually in the process of internally developing trademarks that have been demonstrated to be technically andeconomically feasible Both companies have incurred development costs in the current year with respect to their internally developed trademarks.

Which one of the following best describes how Company A and Company B should account for these development costsin their financial statements?

- A . Company A should expense the development costs while Company B should capitalize the development costs

- B . Company A should capitalize the development costs while Company B should expense the development costs

- C . Both Company A and Company B should capitalize the development costs

- D . Both Company A and Company B should expense the development costs

For a manufacturing company what is the most Importantadvantage of using variable costing rather than absorption costing?

- A . Variable costing includes only variable direct and indirect costs in inventory which makes it more useful for short-term decision making and performance evaluation.

- B . Variable costingis the required inventory method for external reporting in most countries and therefore is less costly to implement

- C . Variable costing is cost-effective and Jess confusing to managers and is therefore more useful in performance evaluation.

- D . Variable costing measures the cost of all manufacturing resources, whether variable or fixed and thus provides the most complete cost.

A company expects sales of 225 000 units in April, 210 000 in May and 190 000 in June.

The company maintains an ending Inventory each month of 25% of the next month’s sales.

How many units should the company plan to produce in May?

- A . 205,000 units.

- B . 210,000 units

- C . 215.000 units

- D . 221,250 units

Which one of the following items is included in accumulated other comprehensive income?

- A . Gains and losses on the sale of equipment

- B . Effect of a change in accounting method

- C . Realized gains on available-for-sale securities

- D . Foreign currency translation adjustments

A building materials retailer uses a LIFO method of valuing its inventory. The company has just introduced a new product.

The following is the activity for the first month of this new product.

• Purchase of 3,000 units on the 2nd of the month at $5.00.

• Purchase of 6,000 units on the 12th of the month at $4.80.

• Purchase of 2,000 units on the 31st of the month at $5 60.

• Sales of the product were 4,000 units on the 20th of the month. Using the periodic method, the ending value of the inventory would be

- A . $34,200.

- B . $35,000.

- C . $35,200.

- D . $35, 800.

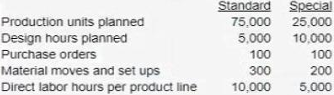

Sportsman inc. manufactures ceramic sports-related figurines. The company’s oldest lines are mass produced in a standard variety of colors and designs. A few years ago in an effort to increase sales, the company began accepting special orders with modified designs in school colors. The minimum order for these special designs is 100 units. The special orders have become very popular and now represent one quarter of the units produced.

Estimates for the year follow.

Design costs manufacturing overhead and materials handling costs are budgeted at $700.000 for the year Sportsman has always used a traditional cost allocation system using aired labor hours as the allocation base but is considering an activity based costing system. The most likely result of changingto an activity-based system is that

- A . the overhead costs allocated to the special designs will likely increase because the special design requires proportionally more overhead activity

- B . the overhead costs allocated to the special designs will likely decrease Because demand for them has grown

- C . total production costs are likely to decline as department are held responsible for their costs

- D . the costs allocated to each product should not change but management will be able to control various components ofthe cost more effectively.

As part of the COSO Internal Control Framework segregation of duties and documentation areincluded in which of the components of the COSO model below?

- A . Operating environment

- B . Risk assessment

- C . Control activities

- D . Information and communication

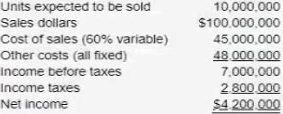

Sullivan Company’s static Budget for the past yearis shown below.

Sullivan actually sow 11.000.000 units throughout the year which was a quantity within its relevant range. The flexible budget net income that should be used to compare to actual results is

- A . $4,200,000.00

- B . $7,500,000.00

- C . $6,580,000.00

- D . $11,500,000.00

GorCo anticipates 10% sales growth each month for the next three months, and plans to sell 120.000 units offinished goods In the first month. The company plans production so that ending inventory is equal to 5% of the next month’s budgeted sales On GorCo’s production budget for the second month the number of finished goods units to be produced would be

- A . 131,340.

- B . 132,000.

- C . 132,600.

- D . 132,660.

Latest CMA Financial Planning Performance and Analytics Dumps Valid Version with 112 Q&As

Latest And Valid Q&A | Instant Download | Once Fail, Full Refund