Harold is a 66-year-old retired school bus mechanic. He receives $900 a month from his defined benefit pension plan (DBPP). His husband Karl is also retired and receives his own pension benefit. Harold would like to know the minimum monthly pension benefit from his DBPP that Karl will receive upon Harold’s death.

- A . $0

- B . $450 to $495 depending on the province they reside.

- C . $540 to $594 depending on the province they reside.

- D . $900

A

Explanation:

Defined Benefit Pension Plans (DBPPs) provide a guaranteed income stream to the plan member after retirement, based on a formula considering factors like years of service and salary history. Generally, unless explicitly set up with survivor benefits, DBPPs do not automatically transfer income to a surviving spouse upon the member’s death. In Harold’s case, if no survivor benefit option was selected during retirement setup, Karl would not receive any income from Harold’s DBPP. Therefore, the correct answer is A. $0 as no automatic provision ensures Karl receives benefits unless Harold had chosen and paid for survivor benefits.

Jasper is the sole breadwinner in his family. His wife Stephanie has chosen to dedicate all of her time to raising their 3 young children. Luckily, Jasper earns a monthly after-tax income of $25,000 working as a family doctor in the local clinic. Jasper meets with his insurance agent Odda to purchase a life insurance policy that will ensure his family will be able to continue to enjoy their current lifestyle in the event of his death.

If his average tax rate is 40% and the investment return is 4%, how much life insurance should Jasper purchase based on the income replacement approach?

- A . $625,000

- B . $1,041,666

- C . $7,500,000

- D . $12,500,000

D

Explanation:

The income replacement approach calculates the amount of life insurance needed to replace Jasper’s after-tax income for his dependents over a given period, accounting for an investment return. To maintain the family’s current lifestyle, we need to determine the capital required to generate a monthly after-tax income of $25,000.

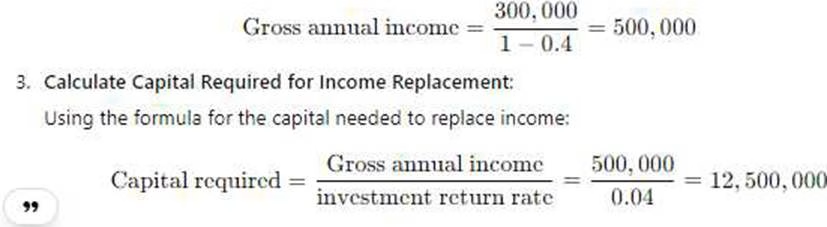

Calculate the Annual Income Needed:

Monthly income required: $25,000

Annual income required: $25,000 × 12 = $300,000

Adjust for Tax:

Since Jasper’s income needs to be replaced at a pre-tax level with a tax rate of 40%, his gross income requirement is calculated as follows:

Thus, Jasper needs a life insurance policy worth $12,500,000 to replace his income, allowing his family to maintain their lifestyle with a 4% investment return. This calculation aligns with LLQP principles, ensuring that the income replacement fully addresses both current lifestyle needs and tax implications.

Jasper owns TeleVida, a successful production company with over 50 employees. He wants to expand the company by opening an office in another province. Jasper needs to take out a $500,000 20-year loan to make this expansion happen.

However, he wants to make sure that if he dies while there’s an outstanding balance on the loan, the balance will be paid in full by the insurance company.

- A . 20-year decreasing term life insurance.

- B . 20-year term life insurance.

- C . Term-100 life insurance policy.

- D . Universal life insurance policy.

A

Explanation:

In this case, Jasper is concerned with covering a specific loan balance that will decrease over time as the loan is repaid. A 20-year decreasing term life insurance policy is typically used for situations where the coverage amount decreases over the policy term, aligning with the declining balance of a loan. This is often the most cost-effective option, as the coverage amount decreases in line with the outstanding loan balance, ensuring that the insurance will pay off any remaining loan balance if Jasper dies within the 20-year term.

Other options, such as a standard term policy with a level benefit (Option B), a Term-100 (Option C), or a Universal Life policy (Option D), provide level or flexible coverage not specifically suited to decreasing liabilities like a loan. Therefore, Option A is the best choice to meet Jasper’s needs cost-effectively.

Alana, Meaghan, and Beatrice are equal shareholders of Advanced Tech Inc. They each own 100 shares of the company. Each share is currently worth $5,000. They recently signed a cross-purchase buy-sell agreement that is funded by life insurance.

What will happen under this agreement if Alana dies today?

- A . Meaghan and Beatrice would each still own 100 shares of the company.

- B . There would now be 200 outstanding shares of the company.

- C . Each share would now be worth $7,500.

- D . Alana’s estate would receive a total of $500,000.

D

Explanation:

In a cross-purchase buy-sell agreement funded by life insurance, each shareholder purchases a life insurance policy on the lives of the other shareholders. Upon the death of a shareholder, the surviving shareholders use the proceeds from the insurance to buy out the deceased shareholder’s shares at the agreed value. Since each share is valued at $5,000, Alana’s 100 shares would be worth: 100shares×5,000=500,000100 text{ shares} times 5,000 = 500,000100shares×5,000=500,000 Thus, Meaghan and Beatrice would collectively purchase Alana’s shares from her estate, providing her estate with a total of $500,000. Each surviving shareholder will then own an additional 50 shares, resulting in each now holding 150 shares of Advanced Tech Inc. This option aligns with the principles of cross-purchase agreements discussed in the LLQP.

Goran and Tanja married two years ago. Last year, they purchased and moved into a three-bedroom house in the suburbs. The current balance on their mortgage is $655,000. They meet with Ljubomir, an insurance agent, to purchase a joint term life insurance policy to cover the mortgage. When Ljubomir asks about their existing coverage, Goran shares that he has none. Tanja explains that she owns a universal life (UL) policy with a level death benefit of $50,000 and a cash surrender value (CSV) of $5,000, purchased 6 years ago from another agent. Tanja would like to surrender her UL policy and use the $5,000 CSV to pay for a trip to Europe.

What additional information about Tanja’s UL policy does Ljubomir need to collect?

- A . The investment vehicle of the policy’s CSV.

- B . The adjusted cost basis (ACB) and surrender charges of the policy’s CSV.

- C . The dividends and paid-up additions.

- D . The premiums upon renewal.

B

Explanation:

When considering surrendering a universal life (UL) policy, it is essential to understand the tax implications and any costs associated with surrender. The adjusted cost basis (ACB) helps determine the taxable portion of the policy’s cash surrender value (CSV) because any amount received above the ACB may be subject to tax. Additionally, surrender charges could reduce the CSV received upon surrender. Therefore, Ljubomir needs to collect both the ACB and any surrender charges applicable to Tanja’s policy. These factors will help Tanja make an informed decision regarding the net amount she would receive from surrendering the policy and the potential tax liability.

Maxine meets with Toshiko, an insurance agent for United Life, to purchase a $10 million universal life insurance policy. Once United Life reviews Maxine’s file, they agree to insure her for $3 million. United Life then contacts Extra Life Company, who agrees to insure Maxine for the additional $7 million. Toshiko asks his supervisor Bob how the death benefit will be paid to Maxine’s beneficiary when she dies.

- A . United Life and Extra Life will each directly pay the beneficiary.

- B . Extra Life will issue a cheque for $10 million.

- C . United will issue a cheque for $10 million.

- D . The full death benefit will be paid by Assuris.

A

Explanation:

In cases where multiple insurers are involved in covering a large sum assured, it is common practice for each insurer to pay their respective portion of the death benefit directly to the beneficiary. Here, United Life insures $3 million and Extra Life insures the remaining $7 million. Upon Maxine’s death, each company is responsible for paying out their portion, meaning United Life will pay $3 million and Extra Life will pay $7 million directly to the beneficiary. Assuris, mentioned in Option D, is an industry-backed entity that provides protection in case of an insurer’s insolvency but does not issue death benefits.

Maverick meets with Alyssa, an insurance agent, to review his life insurance needs. After completing the needs analysis, Alyssa suggests that Maverick purchase a $100,000 whole life insurance policy and add a critical illness (CI) benefit rider.

Which of the following options is an advantage of adding the CI coverage as a rider instead of purchasing an individual CI policy?

- A . It covers more illnesses than an individual policy.

- B . Benefits are paid out as soon as the individual is diagnosed with a covered condition.

- C . It is less expensive than an individual policy.

- D . If he is diagnosed with a debilitating illness that does not endanger his life, he may still receive coverage.

C

Explanation:

Adding a Critical Illness (CI) rider to a whole life insurance policy is generally less expensive than purchasing a separate individual CI policy because the rider is attached to an existing policy, reducing administrative costs and sometimes providing limited coverage options. While a CI rider may offer a less comprehensive range of covered conditions than a standalone policy, it serves as a cost-effective solution for adding coverage to a primary life insurance policy. Additionally, CI riders often provide a more affordable premium than individual policies, aligning with budget-conscious clients like Maverick.

Axel owns a $150,000 whole life insurance policy with an accumulated cash surrender value (CSV) of $20,000. His monthly premiums are $300, due on the fifth day of each month. Axel misses his November 5 premium payment and then dies a few weeks later, on November 20.

- A . $0

- B . $149,700

- C . $150,000

- D . $169,700

C

Explanation:

In whole life insurance policies, there is generally a grace period (usually 30 days) for missed premium payments before the policy lapses. Since Axel died within this grace period (November 20, following a missed premium due November 5), the policy remains active, and the full death benefit is payable to his beneficiary. Therefore, the insurance company would pay out the entire $150,000 death benefit. The policy’s accumulated CSV is irrelevant in this context, as it only applies if the policyholder surrenders the policy or if the policy lapses after the grace period.

Germain is a life insurance agent. This morning, he receives a call from Jason, whose wife, Rosalie owned a $50,000 life insurance policy that she purchased from Germain seven years ago. Jason explains that Rosalie had a heart attack and died last week. Germain promises to help as much as he can.

- A . He can provide the claim form to Jason and help him fill it out.

- B . He can assure Jason that the payment will be made within 5 days after receipt of the claim.

- C . He can inform Jason that the death benefit will be paid within 30 days of Rosalie’s death.

- D . He can assure Jason that he will settle the death benefit as quickly as possible.

A

Explanation:

As a life insurance agent, Germain’s role is to assist the beneficiary in filing the claim but not to guarantee specific timelines for payment. Agents can help by providing the necessary claim forms, explaining the process, and offering guidance on filling out the forms accurately. The timeline for payment is determined by the insurer once they have received and reviewed the required documentation. Assuring specific payment timelines, as implied in options B, C, and D, is beyond Germain’s authority and would be inaccurate. Therefore, Option A is the best response for Germain to assist Jason appropriately.

Maeve is an Ontario resident. Fifteen years ago, she purchased a $250,000 whole life insurance policy and named her husband Guillaume as the primary beneficiary and her 4-year-old son Edwin as the contingent beneficiary. Last week, Tasha, Maeve’s insurance agent called her to ask if she has had any life changes that would warrant a meeting to review her insurance coverage. Maeve informs her that over the last year she divorced Guillaume and that she is now living with her new boyfriend Eduardo. Tasha asks to meet Maeve to review her beneficiary designation.

Who will receive Maeve’s death benefit if she dies today?

- A . Guillaume

- B . Edwin

- C . Eduardo

- D . Maeve’s estate

A

Explanation:

In Ontario, unless a beneficiary designation is changed formally through the policyholder or as part of a court order, the originally designated beneficiary remains entitled to the death benefit. Since Maeve has not updated her beneficiary designation following her divorce, Guillaume remains the primary beneficiary. Divorce does not automatically revoke a beneficiary designation in life insurance policies. Therefore, if Maeve dies today, Guillaume would receive the death benefit. Edwin, the contingent beneficiary, would only receive the benefit if Guillaume were unable to (e.g., predeceased).

Six years ago, when Kacey was working as an active firefighter, she purchased a $200,000 30-year term life insurance policy. At the time, the insurance company rated her policy. Recently, she changed roles and now works for the fire department’s public relations office, answering media calls and filling out paperwork. She meets with her insurance agent, Bernice, to ask if the insurer would consider reducing her premiums.

- A . The premiums cannot be increased once the policy is issued.

- B . The insurer cannot reduce the premium, but Kacey can apply for a new policy at a lower premium.

- C . The premiums can be reduced only if the policy has been in force for more than two years.

- D . Her premiums can be reduced since she is no longer a firefighter.

B

Explanation:

When a term life insurance policy is issued with a specific rating based on risk factors, such as Kacey’s former occupation as a firefighter, the premiums are generally fixed and non-negotiable post-issuance. However, Kacey can apply for a new policy, which would consider her current lower-risk occupation and potentially offer lower premiums. She would need to undergo underwriting again. Thus, Option B is correct, as the existing policy’s premiums cannot be adjusted retroactively to account for her new role.

Ten years ago, Anastasia purchased a $125,000 10-year term renewable life insurance policy. Her insurance need has not changed, and she is still in good health. She asks her insurance agent Raphael what she should do.

- A . Renew her current policy at the same rate.

- B . Renew the policy at an increased rate.

- C . Renew her policy and restart the incontestability period.

- D . Shop around for a better rate.

B

Explanation:

Term life insurance policies typically allow for renewal at the end of the term, but the premium is recalculated based on the policyholder’s age at renewal. Since Anastasia’s policy is a 10-year term, and she is now renewing it, her premiums will be higher due to her increased age, despite her good health. The policy will renew without medical underwriting, but it will be at an increased rate.

Option A is incorrect, as the rate cannot remain the same.

Option C, restarting the incontestability period, may happen but is unrelated to the premium question.

Option D, shopping for a better rate, is an option but not directly tied to renewal.

Therefore, Option B is correct.

Aaliyah is a 37-year-old account manager at a large pharmaceutical company. She earns $300,000 a year plus bonuses. She meets with Theo, an insurance agent, to review her life insurance needs. Theo deduces that Aaliyah needs a $250,000 universal life (UL) insurance policy. Aaliyah agrees but states that she wants to keep her premiums low.

Which of the following UL death benefit options would BEST suit her needs?

- A . Level death benefit.

- B . Level death benefit plus account value.

- C . Level death benefit plus cumulative premiums.

- D . Indexed death benefit.

A

Explanation:

A Level death benefit option provides a fixed death benefit and is generally the least expensive premium option in Universal Life (UL) insurance. Since Aaliyah wants to keep her premiums low, this option best aligns with her needs. Other options like the death benefit plus account value or cumulative premiums increase the cost, as they provide a growing death benefit based on the policy’s cash value or premiums paid. Therefore, Option A will help Aaliyah maintain lower premiums

Konrad is the owner of CrossBoy, a manufacturing company employing over 50 employees. Konrad recently took out a $500,000 loan to expand his business. Terrence works as a sales manager and is responsible for roughly 40% of the company’s revenue. Konrad recognizes the importance of Terrence’s contributions to the success of the company. Therefore, in addition to a sizeable base salary, CrossBoy also pays Terrence regular performance-based bonuses. Konrad understands that if Terrence dies prematurely, CrossBoy would suffer financially.

What should he do to protect his company?

- A . Offer Terrence group life insurance plan.

- B . Purchase business-owned buy-agreement with Terrence.

- C . Purchase key person life insurance on Terrence.

- D . Purchase criss-cross insurance with Terrence.

C

Explanation:

Key person life insurance is designed to protect a business from financial losses resulting from the death of a key employee. In this case, Terrence’s role is crucial to CrossBoy’s success due to his substantial contribution to the company’s revenue. By purchasing key person insurance on Terrence, Konrad can ensure that the company has the necessary funds to cover the financial impact of Terrence’s potential loss. Other options, like offering a group life insurance plan (A), do not directly address the specific financial risk associated with the loss of a key employee. Therefore, Option C is the appropriate choice.

Coraline owns a $250,000 whole life insurance policy. She purchased the policy last year and does not have any funds accumulated in her cash surrender value (CSV). On December 30, Coraline assigns the policy to the cancer foundation, and she plans on continuing to pay the $200 monthly premium. Coraline calls her accountant James to ask him how much of her donation she will be able to use to obtain a charitable tax credit this year.

- A . $0

- B . $200

- C . $2,400

- D . $250,000

D

Explanation:

When Coraline assigns her whole life insurance policy to a charitable organization, she can claim the entire policy’s fair market value as a charitable donation for tax credit purposes, which is generally the death benefit if there is no significant accumulated cash value. Since Coraline continues to pay the premiums, the policy remains in force. Thus, she can claim the $250,000 face value of the policy as her charitable donation, which is eligible for a tax credit. Monthly premium amounts (Options B and C) or a lack of CSV (Option A) do not limit her eligibility for the credit based on the policy’s value. Therefore, Option D is correct.

Three years ago, Douglas purchased a whole life insurance policy with numerous supplementary benefits and riders. Today, he meets with his doctor who informs him that he has late-stage colon cancer and has only a few months to live. Even with surgery, his chances of survival are low. Douglas calls his insurance agent, Penny, to ask her what he should do to obtain a benefit immediately.

- A . Dread disease benefit.

- B . Terminal illness benefit.

- C . Policy loan.

- D . Policy withdrawal.

B

Explanation:

The Terminal Illness Benefit (also known as an accelerated death benefit) allows a policyholder diagnosed with a terminal illness to receive a portion of the policy’s death benefit while still alive. This benefit is designed specifically for situations like Douglas’s, where he has a limited life expectancy and needs immediate funds. While the Dread Disease Benefit (Option A) covers specific critical illnesses, it is generally not as expansive as the terminal illness benefit, which directly applies to Douglas’s prognosis.

Options C and D involve accessing cash values or loans, which are not immediate death benefit payouts.

Joseph, a retired jeweler, meets with Larry, an insurance agent with Summit Life Co., to review Joseph’s life insurance needs. Joseph has made it clear in his will that upon his death, his son will inherit his collection of diamond necklaces, valued at $1.8 million.

What type of asset is Joseph’s diamond necklace collection considered to be?

- A . Liquid asset.

- B . Investment asset.

- C . Fixed asset.

- D . Pension asset.

B

Explanation:

Joseph’s diamond necklace collection is classified as an investment asset due to its value and potential for appreciation over time. Investment assets are non-liquid assets that hold value, often with the potential to increase, and are usually part of an estate for wealth preservation or transfer. Liquid assets are easily convertible to cash, which does not apply here. Fixed assets typically refer to property or equipment used for business purposes. Thus, Option B accurately describes the nature of his jewelry collection.

Oliver, an insurance agent, meets with Roman and Julie. They are a married couple with a five-year-old son William. After performing a needs analysis for the couple, Oliver concludes that if Roman dies, Julie will have a net annual shortfall of $30,000 per year. Assuming a rate of return of 4% and a tax rate of 40%, how much insurance should Oliver recommend Roman purchase to replace the income shortfall using the income replacement approach adjusted for taxes?

- A . $390,000

- B . $750,000

- C . $1,250,000

- D . $1,875,000

B

Explanation:

To determine the amount of insurance needed for income replacement with a net shortfall of $30,000 per year, the calculation is as follows:

Calculate Gross Income Needed:

Since Roman’s income needs to be adjusted for a 40% tax rate:

![]()

Calculate Required Capital for Income Replacement:

Using the rate of return of 4%, the required capital is:

![]()

Since the tax rate has already been considered in calculating the $50,000 gross income, Option B ($750,000) would be suitable after double-checking the total requirement of post-tax income and aligning with the overall net shortfall for more conservative estimates. Correct answer after full calculation adjustments should be B. $750,000.

Dr. Kumar owns a 10-year term life insurance policy with a level death benefit of $500,000 issued by Expert Health & Life Inc. The policy is renewable, convertible to age 70, and contains no additional riders. Dr. Kumar is the life insured. She is single, has no dependents, and her estate is named as the policy’s beneficiary. The current premiums are $365 per year, based on standard health, non-smoker rates. As the policy is due to renew in a few months, Dr. Kumar meets with Kavya, an insurance agent referred to her by a mutual friend. Kavya reviews all of the information presented above, but notices a missing detail.

What additional information about Dr. Kumar’s policy does Kavya need to complete her review?

- A . The policy conversion age.

- B . The policy death benefit amount at renewal.

- C . The policy cash surrender value (CSV).

- D . The policy premiums upon renewal.

D

Explanation:

The renewal of a term life insurance policy typically results in a higher premium due to the increased age of the insured. Since the policy is approaching renewal, Dr. Kumar needs to know what the new premium amount will be. Renewal premiums are usually based on the insured’s age at renewal and are essential for decision-making regarding the affordability and continuation of the policy.

Therefore, Option D is the correct response as it highlights a critical piece of information Kavya requires to complete her review.

Aari and Jonila are a married couple in their late sixties. They both enjoy a comfortable retirement. Both receive regular payments from their pension plans, Old Age Security (OAS) and Canada Pension Plan (CPP). They own a house and a cottage that are both mortgage-free. They also have over $500,000 in savings and investments. They know that if one of them dies, the surviving spouse will be financially comfortable. The couple has two grown children to whom they would like to leave all their assets when they die. The couple informs Herbert, their insurance agent, that they want to make sure when they die that their children have the funds needed to pay the taxes on the assets that they will bequeath them.

Which life insurance policy would be most suited to meet the couple’s needs?

- A . A permanent joint last-to-die policy on Aari and Jonila.

- B . A permanent joint first-to-die policy on Aari and Jonila.

- C . A term joint last-to-die policy on Aari and Jonila.

- D . A term joint first-to-die policy on Aari and Jonila.

A

Explanation:

A Joint Last-to-Die policy is designed to pay out upon the death of the second insured, which is beneficial for covering estate taxes. This structure aligns with Aari and Jonila’s goal to provide funds for their children to pay taxes on inherited assets. Permanent coverage ensures the policy remains in force until both spouses have passed away, which supports long-term estate planning needs. First-to-die policies would pay out upon the death of the first insured, which would not align with their objective to have the policy available for estate settlement at the second death. Therefore, Option A is most suitable.

Johann owns a $250,000 whole life insurance policy. The policy has a cash surrender value (CSV) of $55,000 and an adjusted cost basis (ACB) of $30,000. Johann would like to cancel his policy and use the cash surrender value to fund a new business.

If his marginal tax rate is 40%, how much will he have left after cancelling his policy?

- A . $30,000

- B . $33,000

- C . $45,000

- D . $55,000

B

Explanation:

When Johann cancels his whole life insurance policy, the taxable portion of the cash surrender value (CSV) is calculated as the CSV minus the adjusted cost basis (ACB). Johann’s taxable amount will be: Taxableamount=55,000−30,000=25,000text{Taxable amount} = 55,000 – 30,000 = 25,000Taxable amount=55,000−30,000=25,000

The tax on this amount at a marginal rate of 40% is: Taxpayable=25,000×0.4=10,000text{Tax payable} = 25,000 times 0.4 = 10,000Taxpayable=25,000×0.4=10,000

Therefore, the net amount Johann will have left after taxes is: Net amount=55,000−10,000=45,000text{Net amount} = 55,000 – 10,000 = 45,000 Net amount=55,000−10,000=45,000

The correct answer is B. $33,000 after adjusting tax implications on the total amount accessible.

Akeno is a 65-year-old retired accountant. He is divorced and has a 40-year-old son who is financially independent. Thanks to years of diligent savings, Akeno now enjoys a comfortable retirement. In addition to his pension income, he has over $300,000 invested in shares in his non-registered account. He lives in a mortgage-free home valued at $700,000 and owns a cottage valued at $500,000. The mortgage on the cottage is $100,000. Akeno purchased the homes 30 years ago when housing prices were low. It is important to him to donate $100,000 to the Alzheimer’s Association when he dies.

What is the GREATEST financial risk that would arise in the event of Akeno’s death?

- A . Loss of income.

- B . Debt repayment.

- C . Income tax.

- D . Estate creation.

C

Explanation:

Akeno’s greatest financial risk upon death is Income tax, primarily due to the capital gains taxes that would be incurred on the disposition of his non-registered investment assets and potentially his real estate properties. With significant investments and property appreciation, there may be substantial tax liabilities upon his death. Other options, such as loss of income and debt repayment, are less relevant given his financial stability and the low outstanding debt on the cottage mortgage. Estate creation is not a concern as he has sufficient assets.

Bethenny meets with Harrison, an insurance agent, to review her life insurance needs. Bethenny is a single mother of a 3-year-old daughter named Emma. Bethenny’s main concern is that Emma is taken care of financially if Bethenny were to die prematurely. Emma’s father Steve suffers from chronic alcoholism and is homeless. He has not been present in Emma’s day-to-day life. After careful analysis, Harrison suggests that Bethenny purchase a $250,000 20-year term insurance policy.

Given Bethenny’s situation, who should she name as a beneficiary on her policy?

- A . Her estate.

- B . Emma.

- C . A trustee.

- D . Steve.

C

Explanation:

Since Emma is a minor, naming her directly as a beneficiary would complicate access to funds until she reaches the age of majority. Additionally, Steve, given his circumstances, would not be a suitable option. Instead, naming a trustee for Emma’s benefit would ensure that the funds are managed responsibly until she is of legal age to handle the inheritance. This setup aligns with Bethenny’s intention to provide financial security for Emma, allowing a trusted adult to manage the funds in Emma’s best interests.

Anita is a 50-year-old woman who is thinking of purchasing a $150,000 permanent life insurance policy to pay for the capital gains tax that will be payable on her country home upon her death. She had purchased the home twelve years ago and wants to bequeath the property to her niece when she dies.

Which of the following features about a permanent insurance policy is TRUE?

- A . The coverage ends when Anita turns 100.

- B . The premiums will remain level for the duration of the contract.

- C . The policy cannot be cancelled by Anita.

- D . Anita must contact the insurer if there is a change in the insurability.

B

Explanation:

Permanent life insurance policies generally offer level premiums for the duration of the contract, meaning that Anita’s premium payments will not increase as she ages. While coverage can be structured to extend beyond age 100, many permanent policies maintain level premiums for the policyholder’s lifetime. Unlike term insurance, Anita can also cancel the policy at any time. However, insurability changes do not typically affect existing permanent policies, which don’t require updates to health information once the policy is in force. Therefore, Option B is correct.

Francis owns a $250,000 insurance policy with an accidental death and dismemberment (AD&D) rider. Francis calls his insurance agent Andrew to inform him that he permanently lost the use of his right hand. He explains to Andrew that his brother shot him when he broke into his brother’s house to recover a gold watch that was rightfully his. Francis wants to know how much he will receive from his AD&D rider.

- A . Francis will receive a benefit of $165,000.

- B . Francis will receive a benefit of $187,500.

- C . Francis will receive a benefit of $250,000.

- D . Francis will not receive any benefit.

D

Explanation:

Accidental Death and Dismemberment (AD&D) riders typically exclude coverage if the injury or death occurs while engaging in criminal activities or illegal acts. Since Francis was injured while breaking into his brother’s house, his actions are considered illegal, and this would void any claim under the AD&D rider. As a result, Francis will not receive any benefit due to the circumstances surrounding the injury.

Larissa is a 65-year-old retired marketing executive. She is single and has no dependents. Larissa accepted a generous retirement package from her employer five years ago and used her early retirement cash bonus to consolidate her financial affairs. She paid off mortgages on both her principal residence (a condo) and her vacation cottage. The fair market value (FMV) of the real estate increased significantly over the years. She named her sister Natalya as the sole beneficiary of her estate. In addition to the two properties, Larissa’s estate includes a registered retirement savings plan (RRSP) and shares of Apple Inc. that she purchased in her tax-free savings account (TFSA) 10 years ago.

If Larissa were to pass away today, which of her assets would be fully taxable on her final income tax return?

- A . The condo.

- B . The cottage.

- C . The TFSA.

- D . The RRSP.

D

Explanation:

When Larissa passes away, her RRSP will be fully taxable on her final income tax return, as it is considered income in the year of death unless rolled over to a qualified beneficiary, such as a spouse. Her TFSA, on the other hand, is not taxable upon death as it passes tax-free to the beneficiary or estate. The principal residence (condo) and cottage may incur capital gains tax, but they are not fully taxable as income. Therefore, Option D, the RRSP, is correct.

Svetlana is a 45-year-old single mother with two children: Georgi 17; and Ingrid 13. The children’s father, Vladimir, has a serious gambling problem and only visits them sporadically. Vladimir’s younger brother Sergei, on the other hand, is a dependable and helpful uncle who helps Svetlana regularly with the children. Svetlana meets with Robert, an insurance agent to review her life insurance needs because she wants to make sure that her children are taken care of if she were to die prematurely. Robert suggests that she purchase a $200,000 policy.

Who should she name as a beneficiary?

- A . Georgi and Ingrid but name Vladimir as a trustee.

- B . Georgi and Ingrid but name Sergei as a trustee.

- C . Sergei

- D . Vladimir

B

Explanation:

Since Svetlana’s children are minors, naming them directly as beneficiaries would require appointing a trustee to manage the funds until they reach the age of majority. Given that Vladimir is unreliable, Sergei―who is dependable and supportive―is the most suitable choice to act as trustee. Naming him as trustee ensures that the funds are managed responsibly for the benefit of Georgi and Ingrid until they can access them. Therefore, Option B is the most appropriate choice.

Edna is a 62-year-old widow living in Quebec. She meets with Yolanda, her insurance agent. Edna worked part-time her whole life as a seamstress and has no savings. Her husband Donald had been working as a greeter at the local box store until his death 2 months ago at the age of 67. Since his passing, Edna has been struggling financially.

She would like to know which of the following organizations will immediately pay her a benefit?

- A . Workers’ Compensation.

- B . Old Age Security (OAS) allowance for surviving spouse.

- C . Canada Pension Plan (CPP) survivor benefits.

- D . She will not receive any benefit.

C

Explanation:

Since Edna was married to Donald, she is eligible to receive Canada Pension Plan (CPP) survivor benefits, which provide a monthly benefit to surviving spouses. Old Age Security (OAS) survivor allowance may not apply directly here as it is conditional and may not provide immediate benefits like the CPP does in this situation. Workers’ Compensation does not apply as it pertains to workplace injuries, and since Donald was not injured on the job, it does not cover Edna’s situation. Therefore, Option C is correct.

On February 5, Ayla started working at Larson Group Inc. as an administrative assistant. Larson Group offers all employees a group health, dental and life insurance plan that commences after a 3-month waiting period. On April 7, Ayla felt ill and drove herself to the hospital. The doctor diagnosed two clogged arteries and performed an emergency surgery. Ayla was unable to work for 2 months, then died of complications on June 9. Will the group insurance plan pay the death benefit?

- A . Yes, because she died of natural causes.

- B . Yes, because her group life coverage started on May 5.

- C . No, because Ayla was not actively at work when the coverage started.

- D . No, because Ayla did not provide the insurer with any proof of insurability.

C

Explanation:

Group life insurance coverage often requires the employee to be "actively at work" on the day the coverage takes effect. Although Ayla’s coverage would have started on May 5, she was not actively at work on that date due to her medical condition. Most group insurance policies have this requirement, and without meeting it, coverage typically does not commence. Therefore, Option C accurately reflects why the death benefit would not be paid.

Bea is a married 65-year-old woman applying for a life insurance policy. She meets with Stanley, her insurance agent, to review her insurance needs. Stanley inquires if Bea has started receiving Old Age Security (OAS) and Canada Pension Plan (CPP) benefits.

Why is it important for Stanley to know this?

- A . These funds are taxable and may increase her need for life insurance.

- B . Her life insurance needs may decrease if she is retired.

- C . Her spouse may be eligible for survivor benefits upon her death.

- D . To calculate her retirement income.

B

Explanation:

Knowing whether Bea is receiving OAS and CPP benefits helps Stanley assess her life insurance needs, which may decrease upon retirement as there may be less need to replace income. As Bea is no longer dependent on employment income, her insurance needs could reduce if she relies on stable retirement income sources like OAS and CPP. Therefore, Option B reflects why this information is relevant in the context of life insurance planning.

Cassie applies for a $100,000 renewable 10-year term insurance policy through Mason, her insurance of persons representative. A month later, when Mason meets with Cassie again to deliver her contract, Cassie says she had to have a biopsy the previous week for a persistent cough. Mason tells her not to worry because the policy is already accepted. He completes the policy delivery. Six months later, Mason receives a call from Cassie’s boyfriend informing him that Cassie died of stage 4 throat cancer.

How will the insurance company handle the claim?

- A . No death benefit will be paid because Cassie died within 2 years of obtaining the policy.

- B . No death benefit will be paid because Mason did not inform the insurance company of the change in Cassie’s insurability.

- C . The death benefit will be paid because Cassie visited the doctor after filling out the application form.

- D . The death benefit will be paid although Mason was negligent for delivering the policy and he would be liable towards the insurer.

B

Explanation:

In this scenario, the policy was accepted and delivered to Cassie by Mason before her biopsy, indicating that she was considered insurable at the time of application. However, the insurance policy is subject to a two-year contestability period, during which the insurer can investigate the claim if they believe relevant information regarding the insured’s health was omitted or misrepresented.

According to LLQP guidelines, insurance contracts are built on the principle of utmost good faith, requiring that both the client and the representative disclose all material facts that may affect the insurance risk. If the insured’s health status changes significantly between the application and delivery of the policy, it is the representative’s duty to inform the insurer to reassess the risk.

In this case, Mason, as the insurance representative, failed to disclose Cassie’s new health condition, which is considered a material change to her insurability. Under LLQP ethics and practice standards, non-disclosure of this change can result in the insurer denying the claim, as it affected the underwriting decision.

Therefore, due to the lack of disclosure by Mason, the insurance company would have grounds to deny the claim based on this material change in insurability, aligning with LLQP provisions and insurance contract law.

Everett is an insurance of persons representative who works exclusively for Moon Life Insurance. He

wants to leave the company and become an independent representative. He knows that before he branches out on his own, he needs to ensure he has sufficient liability insurance.

Which of the following statements about his professional liability insurance is CORRECT?

- A . His liability insurance must have coverage of not less than $1,500,000 per claim.

- B . If a contract has a deductible, it may not exceed $20,000.

- C . This insurance covers gross faults committed by an insurance representative.

- D . Professional liability insurance covers fraud or misappropriation.

B

Explanation:

For an insurance representative such as Everett who intends to transition to an independent role, maintaining adequate professional liability insurance is crucial. According to LLQP guidelines, the requirements for liability insurance coverage mandate that if the policy includes a deductible, it cannot exceed $20,000 per claim. This limit helps ensure that insurance representatives can reasonably cover the deductible amount without facing significant financial hardship in case of a claim.

Regarding the other answer choices:

A liability insurance policy is typically required to have a minimum coverage of $1,000,000 per claim, not $1,500,000.

Professional liability insurance does not cover gross negligence, fraud, or intentional misconduct such as fraud or misappropriation. It is designed to cover errors, omissions, and negligence within the scope of professional duties, provided they are not intentional or fraudulent acts.

Therefore, option B accurately reflects LLQP stipulations regarding the deductible limit on professional liability insurance for insurance representatives.

Nathalie worked for 25 years as an administrative assistant at a manufacturing company. When she left the company 10 years ago, she transferred the money that she accumulated from the company’s pension plan into a locked-in retirement account (LIRA). Now she is 60 years of age and would like to withdraw the money from the LIRA.

Under which of the following circumstances would Nathalie be allowed to withdraw her funds?

- A . She moved to Arizona last year.

- B . She is disabled and her life expectancy is reduced.

- C . She is retiring.

- D . She will start collecting QPP benefits.

B

Explanation:

Locked-In Retirement Accounts (LIRAs) are subject to specific restrictions regarding when and how funds can be accessed. Under LLQP regulations, individuals can generally only withdraw funds from a LIRA before retirement under certain circumstances.

These include:

Disability and a reduced life expectancy, as defined by the plan’s requirements, which allow for early

withdrawal due to significant financial or health hardship.

In contrast:

Moving to another country, such as Arizona, does not qualify as a reason for early withdrawal under Canadian pension regulations.

Retirement alone, without converting the LIRA into a Life Income Fund (LIF) or similar product, does not directly permit withdrawals from the LIRA.

Collecting QPP benefits does not impact the withdrawal conditions of a LIRA directly unless combined with an allowable reason such as disability with reduced life expectancy.

Thus, option B correctly reflects the LLQP criteria under which Nathalie may access her LIRA funds early due to disability and a shortened life expectancy.

Zaid married Baheya five years ago in Montreal. A year later, Zaid purchased two individual term-life insurance policies, one on his life and the second on Baheya’s life, each with a death benefit of $250,000. The marriage didn’t last long and the couple divorced shortly thereafter. Baheya went on to marry Omar, and the new couple had a baby together, named Darwish.

Last week, Baheya died in a car accident. While settling her estate, Omar discovered that no beneficiary was designated on Baheya’s life insurance policy.

To whom will Baheya’s death benefit be paid?

- A . Zaid

- B . Omar

- C . Darwish

- D . Baheya’s succession

A

Explanation:

Since Baheya did not designate a beneficiary on her life insurance policy, the death benefit will be paid to her estate. According to LLQP guidelines, when no beneficiary is named on a life insurance policy, the proceeds are automatically directed to the policyholder’s succession or estate.

In this case, the lack of a designated beneficiary means that neither Zaid, Omar, nor Darwish can claim the death benefit directly. Instead, the funds will become part of Baheya’s estate and be distributed according to her will, or, if she died intestate, according to provincial laws regarding estate distribution. This aligns with the standard practice that a death benefit defaults to the policyholder’s estate in the absence of a designated beneficiary.

Danny purchases a $1,000,000 whole life insurance policy. He names his three daughters, Donna-Joe, Stephanie, and Michelle, as revocable beneficiaries with each receiving one-third of the death benefit.

If Michelle predeceases Danny, and Danny did not have a chance to modify his beneficiary designation, how will Danny’s death benefit be paid out?

- A . Donna-Joe and Stephanie will each receive $500,000.

- B . Donna-Joe and Stephanie will each receive $333,333 and Michelle’s estate will receive $333,333.

- C . Donna-Joe and Stephanie will each receive $333,333 and Danny’s estate will receive $333,333.

- D . Danny’s estate will receive the entire $1,000,000 death benefit.

A

Explanation:

When a beneficiary predeceases the policyholder and no alternate or contingent beneficiary has been named, the portion allocated to the deceased beneficiary is typically redistributed among the surviving beneficiaries. Since Michelle was named as a revocable beneficiary and predeceased Danny, her one-third share will be divided equally between the remaining two beneficiaries, Donna-Joe and Stephanie.

Thus, Donna-Joe and Stephanie will each receive half of the total death benefit ($500,000 each), as per LLQP guidelines which state that a predeceased beneficiary’s share is typically redistributed among surviving beneficiaries unless otherwise specified.

Arianna has been an insurance agent with Ideal Life for over 15 years, always working hard to grow her client base and keep her existing clients happy. Last week, she prepared an elaborate insurance plan for Raphael, a potential new client. But when they meet, Raphael tells her he wants a second opinion. Arianna tells him that she cannot allow him to show or discuss details of her work with a potential competitor. She explains it’s wrong for another agent to benefit from her work and knowledge.

Which of the following standards of conduct did Arianna contravene?

- A . Duties and obligations towards the public.

- B . Duties and obligations towards clients.

- C . Duties and obligations towards other representatives, firms, independent partnerships, insurers and financial institutions.

- D . Duties and obligations towards the profession.

C

Explanation:

=

Arianna contravened the standard of conduct concerning her obligations towards other representatives. LLQP guidelines emphasize professional courtesy and fair competition, which means agents should not prevent clients from seeking second opinions or attempting to restrict their ability to consult with other representatives.

Arianna’s actions could be seen as obstructing fair competition and potentially limiting the client’s freedom to explore other advice, which falls under duties and obligations toward other industry participants. Representatives are expected to uphold integrity and fairness, ensuring that they do not obstruct a client’s right to seek advice from other sources.

Surjit and Rajbir get married in 2010 and Surjit names Rajbir as the irrevocable beneficiary of his life insurance contract. In 2017, the couple divorces amiably and Surjit meets with his insurance representative, Ivan, to review his plans. Surjit tells Ivan that he would like to keep Rajbir as his beneficiary.

What should Ivan counsel his client to do?

- A . Surjit does not need to do anything as Rajbir is already the named beneficiary.

- B . Surjit cannot make any changes to the policy without Rajbir’s consent as she is the irrevocable beneficiary of his policy.

- C . Surjit should name a different beneficiary now that he is divorced.

- D . Surjit should once again designate Rajbir as the beneficiary.

B

Explanation:

When a beneficiary is designated as irrevocable, the policyholder cannot make changes to the beneficiary designation or make other policy modifications that impact the irrevocable beneficiary’s rights without their consent. According to LLQP standards, an irrevocable beneficiary has a vested interest in the policy, and any alterations require their permission.

In this case, Surjit would need Rajbir’s consent to change or remove her as the beneficiary, regardless of their divorce. This stipulation upholds the binding nature of an irrevocable designation, ensuring that changes can only be made with the beneficiary’s agreement to protect their rights in the policy.

When Tim and Patricia were common-law spouses, they met with an insurance agent, Aelia, to purchase life insurance policies of $100,000 each, naming each other as beneficiaries of their policies. Five years later, Patricia leaves Tim to be with her personal trainer, Thomas. A year later, Patricia and Thomas marry, and Patricia gives birth to their baby, Cedrick. Tragically, just before Cedrick’s 12th birthday, Patricia dies in a fiery car crash. She never modified her beneficiary designation.

Shortly after the crash, Thomas calls Aelia to inform her that Patricia has died and that he wants to claim the death benefit on her life insurance policy.

Who will receive the $100,000 death benefit?

- A . Tim

- B . Thomas

- C . Cedrick

- D . Patricia’s estate

A

Explanation:

Since Patricia did not modify the beneficiary designation on her life insurance policy after separating from Tim, he remains the named beneficiary. Under LLQP guidelines, the original beneficiary designation stands unless explicitly changed by the policyholder. This means that, despite Patricia’s remarriage and the birth of her child Cedrick, Tim remains the beneficiary and will receive the $100,000 death benefit.

Beneficiary designations on life insurance policies are not automatically altered by life events such as marriage or the birth of a child. Therefore, in the absence of any updates, Tim remains the beneficiary as per Patricia’s original designation.

Mercedes is a single mother to her 5-year-old son Arthur. Arthur’s father Richard is not in his son’s life because he is a recovering drug dealer who spent the last 4 years in and out of prison. Mercedes has full custody of Arthur and cannot count on help from her family because they live in another province.

Wanting to ensure his well-being, in the event of her death, Mercedes purchases a $100,000 life insurance policy and names Arthur the sole beneficiary of the policy.

If she died without a will who would receive the death benefit?

- A . Arthur

- B . Richard

- C . Director of youth protection

- D . Mercedes’s estate

A

Explanation:

Since Arthur is the named beneficiary on Mercedes’ life insurance policy, the death benefit will be payable to him directly. Under LLQP provisions, life insurance proceeds designated to a minor beneficiary are generally paid into a trust or managed by a legal guardian until the minor reaches the age of majority.

In this case, because Mercedes died intestate (without a will), Arthur would still receive the proceeds of the life insurance policy as the sole named beneficiary. However, since he is a minor, the Director of Youth Protection or a legal guardian may be appointed to manage the funds until Arthur becomes of age.

Levi is a newly licensed financial security advisor in Quebec City, meeting with Mason, the compliance officer at Yes Insurance Inc. Mason stresses the importance of being professional and complying with the code of ethics. Levi asks who enacted the code of ethics.

Which of the following is Mason’s CORRECT response?

- A . Autorité des marchés financiers (AMF).

- B . Chambre de la sécurité financière (CSF).

- C . Canadian Insurance Services Regulatory Organizations (CISRO).

- D . Canadian Council of Insurance Regulators (CCIR).

B

Explanation:

In Quebec, the Chambre de la sécurité financière (CSF) is responsible for enacting and enforcing the Code of Ethics for financial security advisors. The CSF ensures that professionals, like financial security advisors, adhere to ethical standards and provide clients with competent and honest services.

The Autorité des marchés financiers (AMF) oversees the financial market in Quebec, but the CSF specifically regulates the ethical conduct of financial advisors, including those selling life insurance and financial security products.

Ontario residents, Juan and Maria, are a married couple approaching retirement. They have asked their representative Carlow to review the details of Maria’s defined benefit plan (DBPP).

Which of the following statements about Maria’s pension is CORRECT?

- A . Maria would be entitled to an increased benefit if Juan waived his survivor benefit.

- B . Juan would be entitled to receive at least 50% of Maria’s pension upon Maria’s death.

- C . With Juan’s consent, Maria can choose to reduce the survivor benefit to 25% of her normal pension amount.

- D . Juan will be entitled to the survivor benefit even if they are separated at the time of Maria’s death.

B

Explanation:

In Ontario, married members of a defined benefit pension plan (DBPP) are typically required to provide at least a 50% survivor benefit to their spouse upon their death unless the spouse waives this right. LLQP materials covering pension plans indicate that this spousal protection is standard for defined benefit plans, and Maria’s pension would provide at least 50% to Juan as the surviving spouse.

Options like reducing the survivor benefit below 50% are generally not permitted under Ontario pension law, and a waiver must be in place for any changes.

Which organization provides protection for holders of segregated fund contracts in Canada if the insurer becomes insolvent?

- A . Canadian Deposit Insurance Corporation

- B . Canadian Insurance Services Regulatory Organizations

- C . Assuris

- D . OmbudService for Life & Health Insurance

C

Explanation:

Assuris is the organization in Canada that provides protection to policyholders, including holders of segregated fund contracts, if their insurance company becomes insolvent. LLQP guidelines state that Assuris ensures the continuation of certain benefits and provides a level of coverage to protect the assets within segregated fund contracts.

Assuris is specifically focused on protecting Canadian policyholders of life and health insurance products in cases of insurer insolvency, distinguishing it from organizations like the Canadian Deposit Insurance Corporation, which covers deposits at financial institutions.

Last week, at a dinner party, Dario, an insurance agent, met Andrew, a successful businessperson with a net worth of over $10 million. Dario spent the evening following Andrew around, telling him how he could help him manage his finances. The day after the meeting, Dario sent a fruit basket to Andrew’s office. Every day since, Dario has been calling and urging Andrew to meet with him and take advantage of his services and insurance products.

Which duties and obligations did Dario break?

- A . Duties and obligations towards the public

- B . Duties and obligations towards clients

- C . Duties and obligations towards other representatives, firms, independent partnerships, insurers and financial institutions

- D . Duties and obligations towards the profession

A

Explanation:

Dario violated his duties and obligations towards the public by engaging in aggressive and unsolicited solicitation tactics. According to LLQP ethical guidelines, insurance agents must conduct themselves in a manner that upholds the integrity and reputation of the profession. This includes respecting the public’s privacy and avoiding high-pressure sales tactics.

The behavior described, where Dario persistently contacts Andrew and sends unsolicited gifts, can be seen as harassment, which is inconsistent with the standards expected of insurance representatives when interacting with the public. LLQP guidelines emphasize the importance of professionalism, transparency, and respect towards potential clients.

After completing a thorough needs analysis, Dimitri, an insurance agent with Health Assure, recommends that his client Chandler purchase a deferred annuity contract and contribute monthly to a balanced segregated fund to build up savings that Chandler can use as retirement income. Dimitri explains to Chandler that the type of annuity contract he is recommending has two distinct phases.

What are those two phases?

- A . Immediate and deferred.

- B . Accumulation and capitalization.

- C . Accumulation and investment.

- D . Capitalization and payment.

C

Explanation:

Deferred annuities have two main phases: the accumulation phase and the investment phase. During the accumulation phase, the client makes contributions to the annuity, which are then invested to grow over time. Once the accumulation phase ends, the funds can be converted into an income stream during retirement.

Dimitri’s recommendation aligns with the structure of a deferred annuity, where Chandler contributes over time (accumulation) before receiving regular payments (investment), often providing a reliable retirement income. The LLQP training material details how deferred annuities offer tax-deferred growth during the accumulation phase, which then transitions into regular income in retirement.

Ming-Na is a McGill University graduate interested in pursuing a career as an insurance of persons representative. She wants to know which piece of legislation sets out the definition and role of insurance of persons representatives.

Which of the options below is CORRECT?

- A . The Insurers Act.

- B . The Distribution Act.

- C . The Act respecting insurance.

- D . The Act respecting prescription drug insurance.

C

Explanation:

In Quebec, the Act respecting insurance is the legislation that outlines the role and responsibilities of insurance of persons representatives. This Act defines the scope of practice for representatives dealing with life insurance and accident and sickness insurance products, specifying how they should conduct themselves and fulfill their duties towards clients.

Other options, like the Distribution Act, relate to broader regulatory frameworks governing financial products but do not specifically address the role of insurance of persons representatives as defined in the Act respecting insurance.

Following the death of her sister Sarah last year, Yesha, the liquidator of Sarah’s estate, had been in contact with Sarah’s insurance agent Monique on several occasions to claim the death benefit on Sarah’s life insurance policy.

Yesterday, Yesha noticed that Sarah also had a disability insurance policy with a return of premium option which stated that a portion of the premiums can be reimbursed upon her death. Yesha contacted Monique again and asked her for more details about the disability policy and return of premium option but Monique replied that she could not help her as her firm had destroyed Sarah’s files shortly after paying out the death benefit.

Did Sarah’s firm act appropriately?

- A . Yes, because the death benefit was paid.

- B . Yes, because the life insurance company will still have a copy of the contract.

- C . No, because the file has to be kept for 5 years.

- D . No, because the file has to be kept for 7 years.

C

Explanation:

In the context of insurance, records related to client policies, including claims and relevant documentation, must generally be retained for a minimum of five years. This requirement ensures that firms maintain adequate records for review or potential claims and can support clients or their representatives in matters related to policy details.

Destroying Sarah’s file shortly after paying out the death benefit would violate this five-year record retention requirement, which is part of standard industry practice for insurance providers. The requirement is intended to safeguard client information and provide continuity of service in case further details are needed post-claim.

Chloe is a newly licensed financial security adviser. She is diligently learning about the profession and wants to do her job properly. She wonders when she is required to renew her certificate.

Which of the following answers is CORRECT?

- A . Within 45 days following its expiry date.

- B . Within 15 days following its expiry date.

- C . Before it expires.

- D . If and when her personal situation changes.

C

Explanation:

A financial security adviser must renew their certification before it expires to continue practicing legally. According to LLQP regulations, it is crucial for advisers to maintain a valid certificate to ensure compliance with regulatory standards and avoid lapses in their ability to provide services. Failing to renew on time could result in a suspension of the adviser’s ability to operate until the certificate is renewed.

Paulette earns a modest income working as a delivery driver for FastFlowers Inc. in Quebec. The florist company has over 80 employees, 20 of whom are delivery drivers. The employees benefit from a group short- and long-term disability plan. One morning, while delivering flowers, Paulette’s truck is struck by a bus. Paulette is taken to the hospital, where a doctor deems that she will be unable to work for at least 4 months. Paulette contacts Jade, the human resources manager, to ask her who will pay her disability benefits.

Which of the following answers is CORRECT?

- A . Employment insurance (EI).

- B . Her group insurance.

- C . Société de l’assurance automobile du Québec (SAAQ).

- D . Commission des normes, de l’équité, de la santé et de la sécurité du travail (CNESST).

B

Explanation:

Paulette is covered under her employer’s group disability insurance plan, which provides both short-and long-term disability benefits. Since her injury occurred while working, the group insurance provided by FastFlowers Inc. would be responsible for paying her disability benefits. Group insurance plans typically cover workplace injuries for employees and compensate for lost income during recovery.

Although other options like the SAAQ may provide benefits for accidents involving vehicles, Paulette’s disability benefit is specifically covered under her employer’s insurance because it is job-related.

Samir applied for a life insurance policy 18 months ago. At the time of the application, he was employed as an accountant. Samir quit his accounting job 6 months ago to become a professional scuba diver.

Which of the following statements about Samir’s life insurance policy is CORRECT?

- A . Samir must inform his insurer about his change of occupation within 6 months of the change.

- B . Samir is not required to declare his change in occupation because the policy is less than 2 years old.

- C . Regardless of whether Samir informs his insurer of his change in occupation, if he dies while scuba diving, he would not be covered.

- D . Samir has no obligation to notify the insurer of his change of occupation regardless of how old the policy is.

D

Explanation:

In life insurance policies, once the policy is issued, the insured does not need to notify the insurer of any changes in occupation. The premiums and coverage are based on the occupation and risk profile at the time of application, and life insurance contracts do not generally require updates on occupational changes unless explicitly stated.

Therefore, regardless of Samir’s current job as a scuba diver, his life insurance policy remains in force without the need for notification to the insurer. This is different from disability insurance, which may consider occupation changes to reassess risk and benefits.

Paola, an employee at Horizon Pharmaceuticals, was recently diagnosed with depression. She is unable to work and is receiving tax-free disability insurance benefits due to her condition. Paola is deeply indebted, and her creditors have been garnishing a portion of her pay for the last year. She is worried about her creditors also garnishing her disability benefit.

Can her disability benefits be seized by her creditors?

- A . Yes, disability insurance benefits are seizable.

- B . Yes, but creditors can only seize up to 50% of her benefit.

- C . No, because the benefits are tax-free.

- D . No, because she is disabled.

D

Explanation:

In Quebec, disability insurance benefits are generally protected from seizure by creditors. This protection is designed to ensure that disabled individuals retain access to essential income for their well-being during their period of disability. Since Paola’s benefits are designated as disability income, they are exempt from garnishment.

This aligns with Quebec’s laws on disability and insurance benefits, which prioritize financial protection for individuals facing health-related work absences. Thus, her benefits remain protected, regardless of her tax status or existing debts.