CIMA CIMAPRA19-F02-1-ENG F2 Advanced Financial Reporting (Online) Online Training

CIMA CIMAPRA19-F02-1-ENG Online Training

The questions for CIMAPRA19-F02-1-ENG were last updated at Dec 28,2025.

- Exam Code: CIMAPRA19-F02-1-ENG

- Exam Name: F2 Advanced Financial Reporting (Online)

- Certification Provider: CIMA

- Latest update: Dec 28,2025

The consolidated statement of profit or loss for VW for the year ended 30 September 20X7 includes the following:

What is VW’s interest cover for the year ended 30 September 20X7?

- A . 4.5

- B . 3.3

- C . 4.1

- D . 5.1

JJ’s current share price is $1.80, with a dividend of $0.20 a share just about to be paid.

Dividends have increased at an average annual growth rate of 4.5% and this is expected to continue into the future.

What is JJ’s cost of equity?

- A . 17.6%

- B . 16.1%

- C . 12.5%

- D . 11.1%

ST has in issue unquoted 7% debentures which were issued at par and are redeemable in 1 year’s time. These debentures cannot be traded. The yield to maturity on these debentures has been calculated at 5%.

Which of the following would explain why the yield to maturity is lower than the coupon?

- A . ST will benefit from the tax relief on the interest payment.

- B . The debentures will be redeemed at a discount to their par value.

- C . The debentures will be redeemed at their par value.

- D . The market value of the debentures must be higher than their par value.

FG has a weighted average cost of capital of 12% based on its existing:

• level of gearing of 30% (measured as debt/(debt + equity)); and

• business operations.

This would be used as an appropriate discount factor to assess which of the following significantprojects?

- A . A project in an industry in which FG does not currently operate, funded wholly by equity.

- B . A project to extend FG’s existing operations, funded wholly by debt.

- C . A project in an industry in which FG does not currently operate, funded 30% with debt and 70% with equity.

- D . A project to extend FG’s existing operations, funded 30% with debt and 70% with equity.

On 30 November 20X9 OPQ acquires a financial asset that is classified as Available for Sale.

Which of the following describes the value of the financial asset on the date of acquisition?

- A . Fair value excluding transaction costs.

- B . Fair value including transaction costs.

- C . Present value including transaction costs.

- D . Present value excluding transaction costs.

XY purchased $100,000 of quoted 8% bonds in the current year which it intends to hold until redemption.

Which of the following identifies the correct classification and subsequent measurement basis for this financial instrument?

- A . A loans and receivables financial asset subsequently measured at fair value with gains and losses in reserves.

- B . A held to maturity financial asset subsequently measured at amortised cost.

- C . A loans and receivables financial asset subsequently measured at amortised cost.

- D . A held to maturity financial asset subsequently measured at fair value with gains and losses in reserves.

AB sold the majority of its operating equipment to LM for cash on 30 December 20X9 and then immediately leased it back under an operating lease.

AB used the cash proceeds from the sale to reduce its long term borrowings significantly.

No early repayment charge was levied by the lender.

Which of the following statements is true in respect of AB’s ratios calculated at 31 December 20X9?

- A . AB’s return on capital employed would be lower as a result of this sale being recorded.

- B . AB’s current ratio would be lower as a result of this sale being recorded.

- C . AB’s non-current asset turnover would be lower as a result of this sale being recorded.

- D . AB’s gearing ratio would be lower as a result of this sale being recorded.

AB acquired a financial investment on 1 January 20X9, incurring $5,000 related agency fees. AB initially classified the investment as held for trading, in accordance with IAS 32 Financial Instruments: Presentation.

Which of the following statements reflects the accounting treatment that AB adopted in respect of this investment when it prepared its financial statements to 31 December 20X9?

- A . Agency fees were recorded as an expense and the gain/loss on the remeasurement of the investment at the year end was recorded in profit or loss for the year.

- B . Agency fees were recorded as an expense and the gain/loss on the remeasurement of the investment at the year end was recorded in other comprehensive income.

- C . Agency fees were added to the cost of the investment and the gain/loss on the remeasurement of the investment at the year end was recorded in profit or loss for the year.

- D . Agency fees were added to the cost of the investment and the gain/loss on the remeasurement of the investment at the year end was recorded in other comprehensive income.

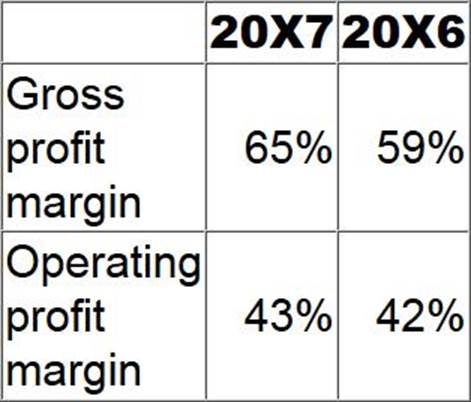

Ratios calculated from the financial statements of ST Group for the years ended 31 August 20X7 and 20X6 are as follows:

Which of the following would have contributed to the movements in these ratios?

- A . During 20X7 ST Group acquired an associate which made a relatively small profit for the year.

- B . ST Group extended its customer base which resulted in an increase in the volume of sales during 20X7.

- C . During 20X7 ST Group increased the useful life of its vehicles to five years from four and adjusted the depreciation charge accordingly.

- D . The fair value of an investment acquired in 20X7 and classified as fair value through profit or loss has increased in value by the year end.

PQ and WX are similar sized entities and operate in the same industry within Country X. Both operate from a single warehouse and have similar levels of non current asset resources.

The following ratios have been calculated at 31 October 20X8:

If considered individually, which of the following would limit the usefulness of these ratios in assessing the comparative financial performances of PQ and WX?

- A . Depreciation of warehouses being charged to cost of sales by PQ and distribution costs by WX.

- B . Operating lease rentals for plant and equipment being charged to administration expenses by PQ and distribution costs by WX.

- C . Year end review of equipment resulting in WX charging an impairment loss while PQ’s equipment is not impaired.

- D . Increased prices for raw materials, which was passed on to customers by both entities.

Latest CIMAPRA19-F02-1-ENG Dumps Valid Version with 248 Q&As

Latest And Valid Q&A | Instant Download | Once Fail, Full Refund