CIMA CIMAPRA19-F02-1-ENG F2 Advanced Financial Reporting (Online) Online Training

CIMA CIMAPRA19-F02-1-ENG Online Training

The questions for CIMAPRA19-F02-1-ENG were last updated at Jan 05,2026.

- Exam Code: CIMAPRA19-F02-1-ENG

- Exam Name: F2 Advanced Financial Reporting (Online)

- Certification Provider: CIMA

- Latest update: Jan 05,2026

EF obtained a government licence, free of charge, to operate a silver mine in 20X7 and $5 million was spent on preparing the site. The mine commenced operation on 1 January 20X8. The licence requires that at the end of the mine’s useful life of 20 years, the site above ground must be reinstated to its original position.

EF estimated that the cost in 20 years’ time of this reinstatement will be $3 million, which has a present value of $1 million at 1 January 20X8.

Which THREE of the following describe how the cost of the reinstatement of the site should be treated in the financial statements of EF in the year ended 31 December 20X8?

- A . The cost of the mine will be increased by $1 million on 1 January 20X8.

- B . The cost of the mine will be increased by $3 million on 1 January 20X8.

- C . There will be a credit to finance costs for the unwinding of the discount on the reinstatement provision.

- D . There will be a debit to finance costs for the unwinding of the discount on the reinstatement provision.

- E . Only the cost of the site preparation will be depreciated over the mine’s useful economic life.

- F . Depreciation will be charged over 20 years on the full cost of the mine including the reinstatement cost.

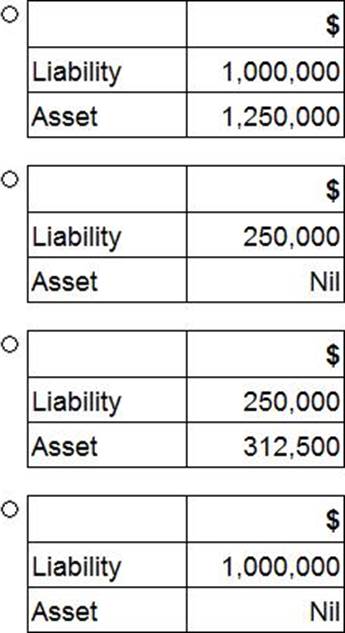

The following information relates to DEF for the year ended 31 December 20X7:

• Property, plant and equipment has a carrying value of $3,500,000 and a tax written down value of $2,500,000.

• There are unused tax losses to carry forward of $1,250,000. These tax losses have arisendue topoor trading conditions which are not expected to improve in the foreseeable future.

• The corporate income tax rate is 25%.

In accordance with IAS 12 Income Taxes, the financial statements of DEF for the year ended 31 December 20X7 would recognise deferred tax balances of:

- A . Option A

- B . Option B

- C . Option C

- D . Option D

GH acquired 3,000,000 of the 12,000,000 equity shares of JK. All shares carried equal voting rights and no other single shareholder of JK held more than 10% of the equity shares. GH has the power to participate in the financial and operating policy decisions but not control them.

Based on the information provided above, how would GH’s investment in JK be accounted for in its consolidated financial statements?

- A . Associate

- B . Joint venture

- C . Joint arrangement

- D . Financial asset

AB acquired its one subsidiary, CD, on 1 January 20X1. At this date the fair value of CD’s property, plant and equipment was found to be $40 million higher than its carrying value. The relevant items had a remaining estimated useful life of 10 years from the date of acquisition.

At 31 December 20X4 AB and CD presented property, plant and equipment of $100 million and $50 million respectively in their individual financial statements.

The value of property, plant and equipment presented in AB’s consolidated statement of financial position at 31 December 20X4 is:

- A . $174 million

- B . $190 million

- C . $150 million

- D . $134 million

ST has in issue unquoted 7% debentures which were issuedat par and are redeemable in 1 year’s time. These debentures cannot be traded. The yield to maturity on these debentures has been calculated at 5%.

Which of the following would explain why the yield to maturity is lower than the coupon?

- A . ST will benefit from the tax relief on the interest payment.

- B . The debentures will be redeemed at a discount to their par value.

- C . The debentures will be redeemed at their par value.

- D . The market value of the debentures must be higher than their par value.

AB, a listed entity, prepared its financial statements to 31 December 20X7, in accordance with international accounting standards.

Which THREE of the following were disclosed as related parties of AB in its financial statements?

- A . AB’s defined benefit pension plan.

- B . The wife of the Managing Director of AB, to whom AB sold a motor vehicle in the year to 31 December 20X7.

- C . ST, an entity that was jointly established by AB and CD, and that is accounted for as a joint venture in AB’s financial statements to 31 December 20X7.

- D . AB’s bank that provides more than 60% of the entity’s loan finance.

- E . AB’s main supplier, GH, who supplies more than 70% of AB’s goods for manufacture.

W and Y are very similar entities with the same level of profit before interest and tax.

However, W has gearing of 95% and Y has gearing of 30%.

Which of the following statements is true?

- A . Investing in W carries a higher level of risk than investing in Y.

- B . A greater proportion of profit will be available out of which to declare a dividend in W.

- C . Investors in Y will expect a higher return than investors in W.

- D . Y has a greater commitment to meet interest payments than W.

RS has issued an instrument with a nominal value of $1 million, at a discount of 2.5%, and a coupon rate of 6%. The terms of the issue are that the instrument must either be redeemed at par, at the option of the holder, in three years’ time, or alternatively converted into equity shares in RS.

The characteristics of this instrument taken as a whole indicates that it would be classifed as which of the following?

- A . Compound instrument

- B . Debt instrument

- C . Equity instrument

- D . Discounted instrument

AB and CD are competitors supplying components to the car manufacturing industry. AB operates in Country X and CD operates in Country

Y. Both entities were incorporated on the same day, are the same size and prepare financial statements to 31 March each year using international accounting standards.

Which of the following statements taken individually would limit the usefulness of the comparison of the return on capital employed ratio between the two entities?

- A . The corporate tax rate is 25% in Country X and 40% in Country Y.

- B . The average rate of inflation is 3% in Country X and 10% in Country Y.

- C . The average rate of borrowing is 2% in Country X and 7% in Country Y.

- D . The currency is Dollar in Country X and Krona in Country Y.

Which of the following defines the calculation of interest cover?

- A . Profit before interest and tax divided by finance costs

- B . Finance costs divided by profit before interest and tax

- C . Profit after tax divided by finance costs

- D . Finance costs divided by profit after tax

Latest CIMAPRA19-F02-1-ENG Dumps Valid Version with 248 Q&As

Latest And Valid Q&A | Instant Download | Once Fail, Full Refund