CIMA CIMAPRA19-F02-1-ENG F2 Advanced Financial Reporting (Online) Online Training

CIMA CIMAPRA19-F02-1-ENG Online Training

The questions for CIMAPRA19-F02-1-ENG were last updated at Dec 18,2025.

- Exam Code: CIMAPRA19-F02-1-ENG

- Exam Name: F2 Advanced Financial Reporting (Online)

- Certification Provider: CIMA

- Latest update: Dec 18,2025

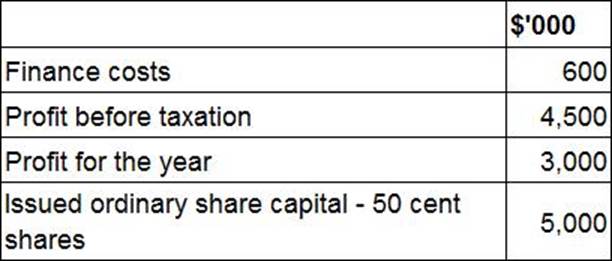

Information from the financial statements of RST for the year ended 30 April 20X9 is as follows:

What is the price earnings (P/E) ratio for RST at 30 April 20X9?

- A . 15.83

- B . 7.92

- C . 10.56

- D . 9.31

LM acquired 80% of the equity shares of ST when ST’s retained earnings were $50 million.

The fair value of the net assets of ST included a contingent liability with a fair value of $100 million at the date of acquisition and a fair value of $40 million at 31 December 20X6.

No other fair value adjustments were required at the date of acquisition.

LM and ST had retained earnings of $200 million and $80 million respectively at 31 December 20X6.

The consolidated retained earnings of LM at 31 December 20X6 were:

- A . $164 million

- B . $176 million

- C . $272 million

- D . $284 million

When accounting for a finance lease under IAS 17 Leases, which TWO of the following are recognised in the statement of profit or loss?

- A . Finance cost element of the lease payments

- B . Depreciation of the leased asset

- C . Lease payments paid

- D . Lease payments payable

- E . Capital repayment element of the lease payments

CORRECT TEXT

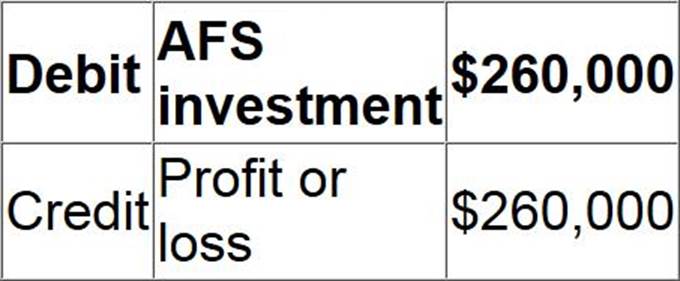

KL acquired 2 million $1 equity shares in MN on 18 July 20X0 for $1.65 a share and classified this investment as available for sale (AFS) in accordance with IAS 39 Financial instruments: Recognition and Measurement.

KL paid a 0.5% transaction fee to its broker on this transaction. MN’s shares were trading at $1.78 on 31 December 20X0.

Which of the following journals records the subsequent measurement of this investment at 31 December 20X0?

GH owned 70% of the equity share capital of XY at 1 January 20X6. GH acquired a further 20% of XY’s equity share capital on 31 December 20X6 for $430,000. Non controlling interest was measured at $600,000 immediately prior to the 20% acquisition.

Which of the following amounts will GH debit to non controlling interest when the 20% acquisition is adjusted for in its consolidated financial statements at 31 December 20X6?

- A . $400,000

- B . $120,000

- C . $200,000

- D . $430,000

How would KL account for its investment in MN in its consolidated financial statements for the year to 31 December 20X9?

- A . Joint venture

- B . Joint arrangement

- C . Financial asset

- D . Subsidiary

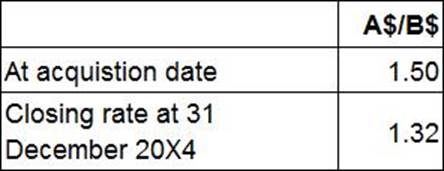

A group presents its financial statements in A$.

The goodwill of its only foreign subsidiary was measured at B$100,000 at acquisition.

There have been no impairments to this goodwill.

Exchange rates (where A$/B$ is the number of B$’s to each A$) are as follows:

The value of goodwill to be included in the group’s statement of financial position in respect of its foreign subsidiary for the year ended 31 December 20X4 is:

- A . A$75,758.

- B . A$66,667.

- C . A$150,000.

- D . A$132,000.

ST acquired 75% of the 2 million $1 equity shares of CD on 1 January 20X3, when the retained earnings of CD were S3,550,000. CD has no other reserves.

ST paid $5,600,000 for the shares in CD and the non controlling interest was measured at its fair value of S1,400,000 at acquisition.

At 1 January 20X3, the fair value of CD’s net assets were equal to their carrying amount, with the exception of a building. This building had a fair value of $1,000,000 in excess of its carrying amount and a remaining useful life of 25 years on 1 January 20X3.

At 31 December 20X5, the retained earnings of ST and CD were $8,500,000 and $5,250,000 respectively.

What is the value of retained earnings that will be presented in the consolidated statement of financial position of ST as at 31 December 20X5?

- A . $9,685,000

- B . $9,775,000

- C . $9,715,000

- D . $10,080,000

On 1 January 20X1 KL acquired 75% of the equity shares of PQ. Goodwill arising on the acquisition was $480,000. On 31 December 20X3 KL sold the full investment of PQ to XY Group for $2,000,000. On this date the net assets of PQ were $1,340,000 and the non-controlling interests stood at $410,000.

What is the gain on disposal to be recognised in the consolidated statement of profit or loss of KL?

- A . $590,000

- B . $180,000

- C . $660,000

- D . $635,000

AB and CD are separate entities that prepare financial statements to 31 May using international accounting standards. AB and CD provide technical support services to the financial services industry and operate in the same country.

The financial statements are identical except for the following:

• AB purchased all operating equipment, paying $100,000, using a 5 year bank loan. The useful life of the equipment was 5 years.

• CD signed an operating lease agreement for all operating equipment for 5 years paying $20,000 per year.

Both entities charge all expenses relating to the equipment to cost of sales.

From the information provided, which of the following ratios would be reliably comparable for AB andCD?

- A . Gross profit margin

- B . Return on capital employed

- C . Non current asset turnover

- D . Profit before tax margin

Latest CIMAPRA19-F02-1-ENG Dumps Valid Version with 248 Q&As

Latest And Valid Q&A | Instant Download | Once Fail, Full Refund