CIMA CIMAPRA19-F02-1-ENG F2 Advanced Financial Reporting (Online) Online Training

CIMA CIMAPRA19-F02-1-ENG Online Training

The questions for CIMAPRA19-F02-1-ENG were last updated at Apr 22,2025.

- Exam Code: CIMAPRA19-F02-1-ENG

- Exam Name: F2 Advanced Financial Reporting (Online)

- Certification Provider: CIMA

- Latest update: Apr 22,2025

On 1 January 20X4 JK had 1,500,000 ordinary shares in issue. On 1 September 20X4 JK issued 600,000 ordinary shares at the market value of $2.50 a share. For the financial year ended 31 December 20X4 the statement of profit or loss shows profit before tax of $625,000 and profit after tax of $500,000.

What is the earnings per share for the year ended 31 December 20X4?

- A . 23.8 cents

- B . 36.8 cents

- C . 26.3 cents

- D . 29.4 cents

Which TWO of the following statements about bonds and their issue are true?

- A . Credit rating agencies assign risk categories to bond issues.

- B . Bonds are a form of loan capital, traded on stock exchanges.

- C . Bonds are a risk-free form of investing because they will always be repaid.

- D . All bonds have the same terms and conditions when issued.

- E . A bond issue is never underwritten because the return is fixed and guaranteed.

CORRECT TEXT

LK acquired 100% of the equity shares of TU on 1 January 20X4. LK disposed of 60% of TU for £2,400,000 on 30 September 20X4. The sale proceeds reflected the fair value of TU’s shares on that date.

The remaining 40% shareholding gave LK the ability to exercise significant influence

over the activities of TU. TU reported profit of $1,800,000 for the year ended 31 December 20X4 and this accrued evenly throughout the year.

Calculate the investment in associate that will be presented in LK’s consolidated statement of financial position as at 31 December 20X4.

Give your answer to the nearest whole $’000.

$ 000

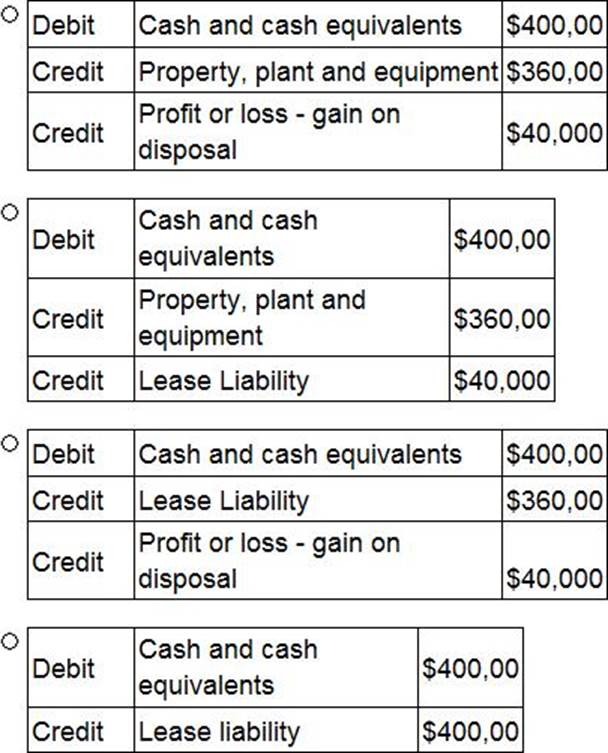

ST has sold its main office property, which had a carrying value of $360,000, to AB, a property management entity.

The property was sold for $400,000 which is equal to its fair value and was immediately leased back under an operating lease agreement.

Which of the following journals will record this transaction?

- A . Option A

- B . Option B

- C . Option C

- D . Option D

Which of the following options provides a representation of how the non controlling interest in FG is measured in CD’s consolidated statement of financial position at 31 December 20X8?

- A . • FV of NCI at acquisition; plus

• NCI’s share of post acquisition reserves of FG; plus

• NCI’s share of accumulated exchange differences arising on goodwill of FG. - B . • FV of NCI at acquisition; plus

• NCI’s share of post acquisition reserves of FG; plus

• NCI’s share of exchange difference arising on goodwill of FG for the year. - C . • FV of NCI at reporting date; plus

• NCI’s share of post acquisition reserves of FG; plus

• NCI’s share of exchange difference arising on goodwill of FG for the year. - D . • FV of NCI at reporting date; plus

• NCI’s share of group reserves; plus

• NCI’s share of accumulated exchange differences arising on goodwill of FG.

As at 31 October 20X7 TU’s financial statements show the entity having profit after tax of $600,000 and 900,000 $1 ordinary shares in issue. There have been no issues of shares during the year. At 31 October 20X7 TU have 300,000 share options in issue, which allow the holders to purchase ordinary shares at $2 a share in 3 years’ time. The average price of the ordinary shares throughout the year was $5 a share.

What is the diluted earnings per share for the year ended 31 October 20X7?

- A . 66.7 cents

- B . 58.8 cents

- C . 50.0 cents

- D . 55.6 cents

On 30 November 20X9 OPQ acquires a financial asset that is classified as Available for Sale.

Which of the following describes the value of the financial asset on the date of acquisition?

- A . Fair value excluding transaction costs.

- B . Fair value including transaction costs.

- C . Present value including transaction costs.

- D . Present value excluding transaction costs.

GG’s gearing is currently 50% compared to the industry average of 40% (both measured as debt/equity). GG’s debt is all in the form of a single bank loan that is repayable in five years’ time. The directors of GG are seeking to raise finance for a new project and they are considering an additional bank loan from the same bank.

Which of the following would prevent the bank from lending the finance for the project in the form of a new bank loan?

- A . A covenant on the existing bank loan that restricts the level of dividend that can be paid.

- B . A projected decrease in interest cover that would breach a covenant on the existing loan.

- C . The revaluation of GG’s property that shows an increase in its value since the existing bank loan was taken out.

- D . A projected lack of profits to be able to claim tax relief on the additional interest arising from the new loan.

CORRECT TEXT

YZ issued $100,000 6% convertible bonds at par on 1 January 20X5. The bondholders have the option to convert into equity shares in 3 years’ time or redeem at par for cash on the same date.

Interest is paid annually in arrears and bonds issued by similar entities without conversion rights pay interest at 8%.

What is the value of equity to be recognised in YZ’s statement of financial position as at 31 December 20X5?

Give your answer to the nearest whole $.

$?

Taking each statement individually, which of the following explains the movement in the gross profit margin from 20X4 to 20X5 as calculated by the analysts?

- A . Increase in the levels of closing inventory of raw materials.

- B . Reduction in the cost of raw materials NOT passed onto customers.

- C . Prompt payment discounts no longer offered to customers.

- D . Increase in the volume of sales over the year.

Latest CIMAPRA19-F02-1-ENG Dumps Valid Version with 248 Q&As

Latest And Valid Q&A | Instant Download | Once Fail, Full Refund