CIMA CIMAPRA19-F01-1-ENG F1 Financial Reporting (Online) Online Training

CIMA CIMAPRA19-F01-1-ENG Online Training

The questions for CIMAPRA19-F01-1-ENG were last updated at Apr 26,2025.

- Exam Code: CIMAPRA19-F01-1-ENG

- Exam Name: F1 Financial Reporting (Online)

- Certification Provider: CIMA

- Latest update: Apr 26,2025

Which of the following is a characteristic of a defined contribution post-employment benefit scheme?

- A . The amount of the post-employment benefits paid to former employees depends on how well the scheme’s investments have performed.

- B . The employer would make additional contributions into the scheme if the actuary predicted a shortfall in the funds available to pay post-employment benefits.

- C . The amount of the post-employment benefits paid to former employees is determined at the date of their retirement using a predefined formula.

- D . The employer may take a contributions holiday and stop paying contributions for a period, if the scheme’s assets appear to be more than are required to meet the scheme’s obligations.

Which of the following is a characteristic of a defined contribution post-employment benefit scheme?

- A . The amount of the post-employment benefits paid to former employees depends on how well the scheme’s investments have performed.

- B . The employer would make additional contributions into the scheme if the actuary predicted a shortfall in the funds available to pay post-employment benefits.

- C . The amount of the post-employment benefits paid to former employees is determined at the date of their retirement using a predefined formula.

- D . The employer may take a contributions holiday and stop paying contributions for a period, if the scheme’s assets appear to be more than are required to meet the scheme’s obligations.

PQ uses the fair value method for non-controlling interest at acquisition.

What is the value of the unrealized profit in inventory adjustment required to inventory in PQ’s consolidated statement of financial position at 31 December 20X0?

- A . $3,333

- B . $2,000

- C . $4,000

- D . $1,667

What does the exemption method of giving double taxation relief mean?

- A . The countries agree that all types of income will be exempt or partially exempt in one country or the other.

- B . The countries agree on certain types of income which will be exempt or partially exempt in one country or the other.

- C . The countries agree on certain types of income which will be exempt or partially exempt in both countries.

- D . The countries agree that all types of income will be exempt or partially exempt in both countries.

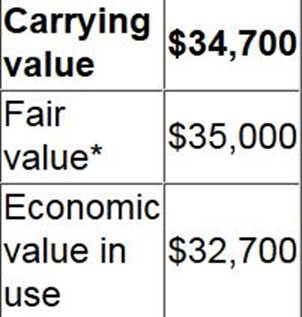

An asset has the following values:

If the asset was sold for its fair value, selling costs of $1,500 would be incurred.

Which of the following is the value of the impairment loss to be recognised for this asset in accordance with IAS 36 Impairment of Assets?

- A . $0

- B . $300

- C . $1,200

- D . $2,000

In most developed countries employers deduct the tax from employees’ pay each month and then pay the tax to the tax authorities on behalf of the employee on a monthly basis.

Which THREE of the following are advantages of this system to the employee?

- A . The tax is collected earlier than systems that assess earnings at the end of the year.

- B . The payment of tax is easier as the tax is deducted before the net salary is paid to the employee.

- C . Most of the administration costs are borne by the employees.

- D . The responsibility for the tax calculations rests with the employer and therefore there is less chance of mistakes being made.

- E . There is less chance of interest and penalties being levied on the employee by the tax

authorities.

A building was purchased on 1 January 20X1 for $300,000 and had a useful economic life of 40 years. On 1 January 20X5 the building was revalued by a professional surveyor at $450,000. Directors decided to incorporate the revalued amount into the financial statements.

The accounting entries to record the initial revaluation of the building in the financial statements for the year ended 31 December 20X5 will be to debit building cost $150,000 and then:

- A . credit accumulated depreciation $37,500 and credit revaluation reserve $112,500.

- B . credit accumulated depreciation $30,000 and credit revaluation reserve $120,000.

- C . debit accumulated depreciation $30,000 and credit revaluation reserve $180,000.

- D . debit accumulated depreciation $37,500 and credit revaluation reserve $187,500.

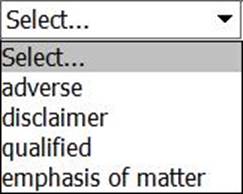

HOTSPOT

Whilst undertaking an external audit, the auditor has identified that there is insufficient evidence to support the financial statements.

As a result the auditors consider these financial statements to be wholly unreliable for decision making purposes.

This will result in a modified audit report with the opinion being.

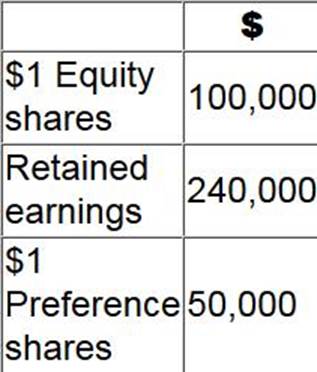

WX is considering an investment in ST.

At 31 December 20X2 ST had the following balances in its statement of financial position:

Which of the following would cause ST to become an associate investment of WX?

- A . WX purchases 15,000 of ST’s $1 equity shares and 20,000 of ST’s $1 preference shares.

- B . WX purchases 25,000 of ST’s $1 equity shares.

- C . WX purchases 75,000 of ST’s $1 equity shares.

- D . WX purchases 50,000 of ST’s $1 preference shares.

Which THREE of the following matters should an entity consider when determining the credit terms granted to a customer?

- A . Typical credit terms operating within the industry

- B . Risk of non-payment

- C . Selling price of the goods being sold to the customer

- D . Bargaining power of the customer

- E . Number of suppliers

- F . Discount offered by suppliers for early payment

Latest CIMAPRA19-F01-1-ENG Dumps Valid Version with 177 Q&As

Latest And Valid Q&A | Instant Download | Once Fail, Full Refund