CIMA CIMAPRA19-F01-1-ENG F1 Financial Reporting (Online) Online Training

CIMA CIMAPRA19-F01-1-ENG Online Training

The questions for CIMAPRA19-F01-1-ENG were last updated at Apr 22,2025.

- Exam Code: CIMAPRA19-F01-1-ENG

- Exam Name: F1 Financial Reporting (Online)

- Certification Provider: CIMA

- Latest update: Apr 22,2025

Country X levies corporate income tax at a rate of 25% and charges income tax on all profits irrespective of whether they are distributed by way of dividend. Country Y levies corporate income tax at a rate of 20%.

A, who is resident in Country X, pays a divided to B, who is resident in Country Y. B is required to pay corporate income tax on the dividend received from A, but a deduction can be made for the tax suffered on this dividend restricted to a rate of 20%.

Which method of relief for foreign tax does this describe?

- A . Exemption

- B . Deduction

- C . Tax credit

- D . Restricted

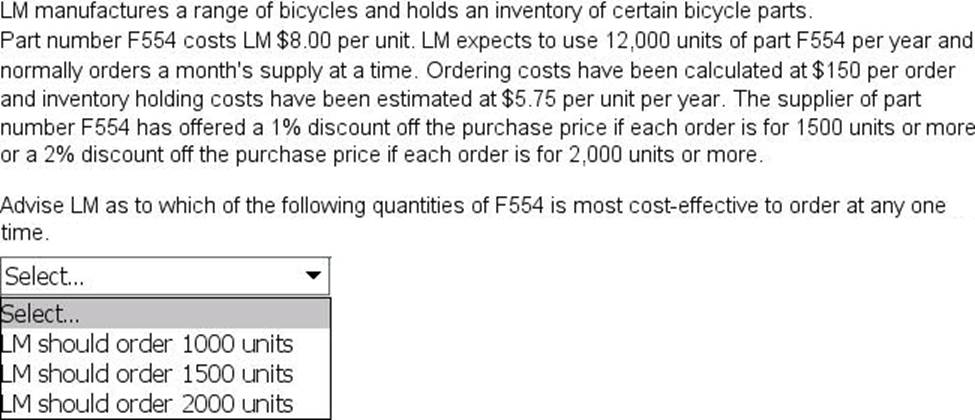

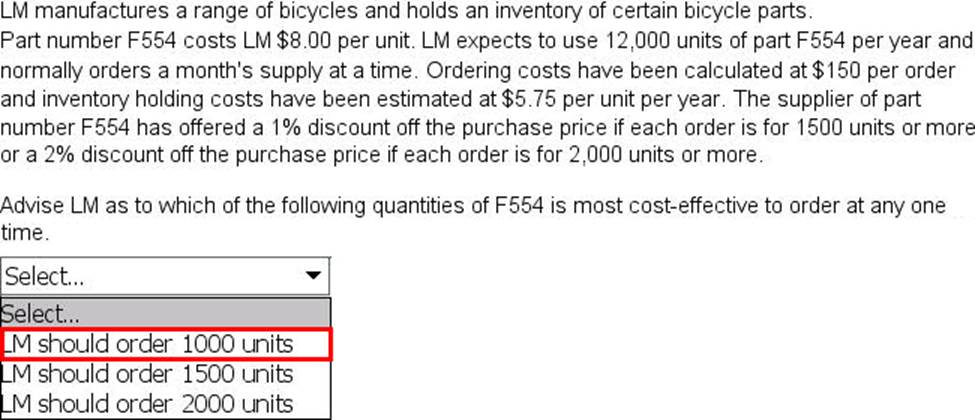

CORRECT TEXT

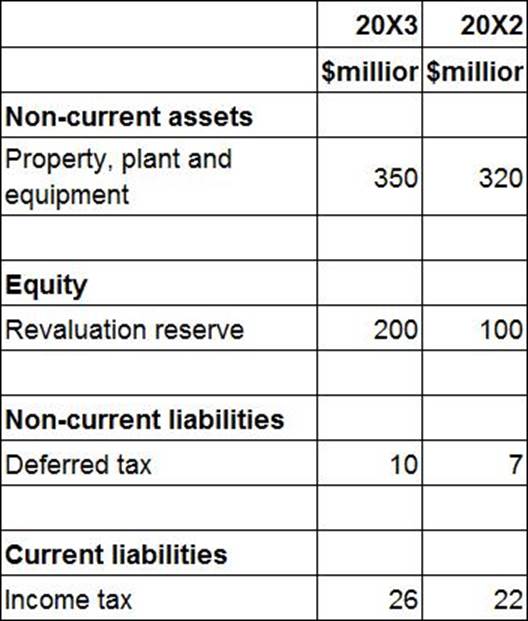

The following information is extracted from the statement of financial position for ZZ at 31 March 20X3:

Included within cost of sales in the statement of profit or loss for the year ended 31 March 20X3 is $20 million relating to the loss on the sale of plant and equipment which had cost $100 million in June 20X1.

Depreciation is charged on all plant and equipment at 25% on a straight line basis with a full year’s depreciation charged in the year of acquisition and none in the year of sale.

The revaluation reserve relates to the revaluation of ZZ’s property.

The total depreciation charge for property, plant and equipment in ZZ’s statement of profit of loss for the year ended 31 March 20X3 is $80 million.

The corporate income tax expense in ZZ’s statement of profit or loss for year ended 31 March 20X3 is $28 million.

ZZ is preparing its statement of cash flows for the year ended 31 March 20X3.

What figure should be included for corporate income tax paid in order to arrive at the net cash flow from operating activities?

Give your answer to the nearest $ million.

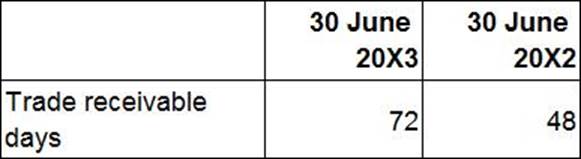

The following information relates to ABC.

Which of the following would be a reason for the movement in the trade receivable days?

- A . A new credit controller was appointed during the year ended 30 June 20X3 who has been chasing customers for payment.

- B . A system of early settlement discount was introduced during the year ended 30 June 20X3 which was taken up by quite a few customers.

- C . One customer who regularly took 120 days to pay their invoices stopped buying goods from ABC during the year ended 30 June 20X3.

- D . It was decided during the year ended 30 June 20X3 to stop undertaking credit checks on new customers.

CORRECT TEXT

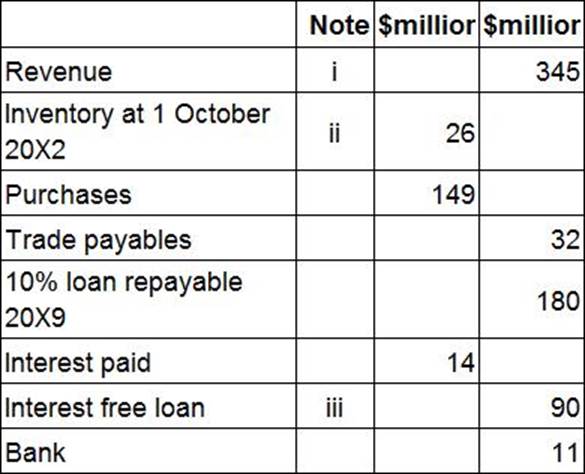

The following information is extracted from the trial balance of YY at 30 September 20X3.

i. Included in revenue is a refundable deposit of $20 million for a sales transaction that is due to take place on 14 October 20X3.

ii. The cost of closing inventory is $28 million, however, the net realisable value is estimated at $25 million.

iii. The interest free loan was obtained on 1 January 20X3. The loan is repayable in 12 quarterly installments starting on 31 March 20X3. All installments to date have been paid on time.

Calculate the figure that should be included within non-current liabilities in YY’s statement of financial position at 30 September 20X3 in respect of both of the loans outstanding at the year end?

Give your answer to the nearest $ million.

Which of the following is a feature of a direct tax?

- A . The formal incidence and effective incidence are usually the same.

- B . It is levied on one part of the economy with the intention that it will be passed on to another.

- C . It is not levied on the eventual payer of the tax.

- D . It cannot be related to the individual circumstances of the tax payer.

Which of the following is a feature of a direct tax?

- A . The formal incidence and effective incidence are usually the same.

- B . It is levied on one part of the economy with the intention that it will be passed on to another.

- C . It is not levied on the eventual payer of the tax.

- D . It cannot be related to the individual circumstances of the tax payer.

Which of the following is a feature of a direct tax?

- A . The formal incidence and effective incidence are usually the same.

- B . It is levied on one part of the economy with the intention that it will be passed on to another.

- C . It is not levied on the eventual payer of the tax.

- D . It cannot be related to the individual circumstances of the tax payer.

Which of the following is a feature of a direct tax?

- A . The formal incidence and effective incidence are usually the same.

- B . It is levied on one part of the economy with the intention that it will be passed on to another.

- C . It is not levied on the eventual payer of the tax.

- D . It cannot be related to the individual circumstances of the tax payer.

Which of the following is a feature of a direct tax?

- A . The formal incidence and effective incidence are usually the same.

- B . It is levied on one part of the economy with the intention that it will be passed on to another.

- C . It is not levied on the eventual payer of the tax.

- D . It cannot be related to the individual circumstances of the tax payer.

Latest CIMAPRA19-F01-1-ENG Dumps Valid Version with 177 Q&As

Latest And Valid Q&A | Instant Download | Once Fail, Full Refund