CIMA CIMAPRA17-BA2-1-ENG BA2 – Fundamentals of Management Accounting (2017 SYLLABUS) (Online) Online Training

CIMA CIMAPRA17-BA2-1-ENG Online Training

The questions for CIMAPRA17-BA2-1-ENG were last updated at Dec 13,2025.

- Exam Code: CIMAPRA17-BA2-1-ENG

- Exam Name: BA2 - Fundamentals of Management Accounting (2017 SYLLABUS) (Online)

- Certification Provider: CIMA

- Latest update: Dec 13,2025

CORRECT TEXT

A company operates a full cost system of pricing. Production overheads are absorbed using a pre-determined absorption rate of £3.50 per machine hour. The direct production cost of product A is £15 per unit and it utilises 6 machine hours per unit. The mark-up for non-production costs is 10% of total production cost. The company wants to make a 25% return on sales revenue for all products.

The required selling price for Product A, to two decimal places, is:

CORRECT TEXT

A product sells for £10 per unit and has an annual break-even volume of 50,000 units. The annual fixed costs are £100,000.

The variable cost per unit is:

Give your answer to 2 decimal places.

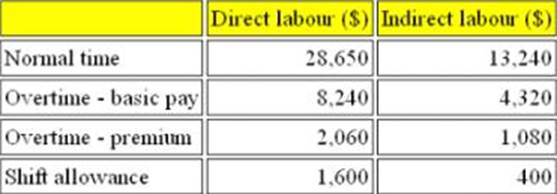

Refer to the exhibit.

The wages analysis for the welding department of a manufacturing company is given below:

What is the direct labor cost for the welding department?

- A . $40,550

- B . $36,890

- C . $30,250

- D . $38,490

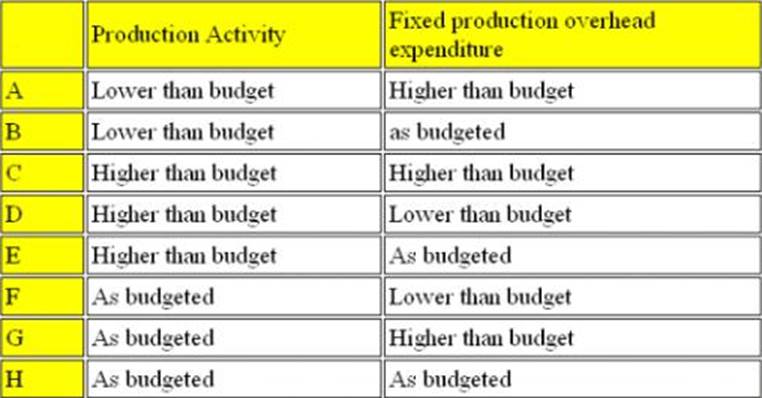

Refer to the Exhibit.

A company operates an absorption costing system. The management accounts show that fixed production overheads were over-absorbed in the period.

Which FOUR combinations could possibly have resulted in this situation?

- A . Combination A

- B . Combination B

- C . Combination C

- D . Combination D

- E . Combination E

- F . Combination F

- G . Combination G

- H . Combination H

The principal budget factor can be defined as:

- A . The factor which has the highest value in the budget

- B . The factor which limits the activities of the organisation

- C . The factor which is most likely to result in an adverse variance

- D . The factor which is least likely to change in the future

CORRECT TEXT

Apex Plc has budgeted to sell 8,000 units of A in the year. Opening inventory of A is estimated at 1,000 units and the company plans to reduce inventory levels of all products by 15%.

What will be the production budget (in units) for the year?

CORRECT TEXT

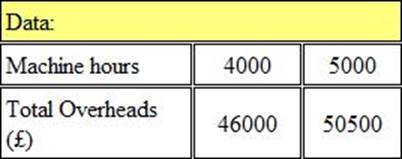

Refer to the Exhibit.

PJ Ltd has forecast that the relationship between total overheads and machine hours will be as follows:

If the budget is to be based on 4,000 machine hours, the variable overhead absorption rate will be:

*per machine hour.

Give your answer to 2 decimal places.

Which of the following industries would not use process costing?

- A . Brewing

- B . House-building

- C . Chemical

- D . Food processing

FL uses an absorption costing system. The overhead absorption rate for production overheads is $8.60 per direct labour hour.

Budgeted production overhead costs for the year were $473,000 and actual costs incurred were $468,000. 56,000 labour hours were used.

Which ONE of the following statements is correct?

- A . Overheads were under-absorbed by $5,000

- B . Overheads were over-absorbed by $8,600

- C . Overheads were under-absorbed by $8,600

- D . Overheads were over-absorbed by $13,600

A company operates an absorption costing system. Overheads are absorbed using a pre-determined absorption rate using labour hours.

Actual labour hours were 10% below budget for the period and overheads incurred were 10% above budget for the period. This would result in:

- A . An over-absorption of overheads for the period

- B . An under-absorption of overheads for the period

- C . Neither an over- or under-absorption of overheads for the period

- D . Impossible to tell from the information available

Latest CIMAPRA17-BA2-1-ENG Dumps Valid Version with 392 Q&As

Latest And Valid Q&A | Instant Download | Once Fail, Full Refund