CIMA CIMAPRA17-BA2-1-ENG BA2 – Fundamentals of Management Accounting (2017 SYLLABUS) (Online) Online Training

CIMA CIMAPRA17-BA2-1-ENG Online Training

The questions for CIMAPRA17-BA2-1-ENG were last updated at Jan 06,2026.

- Exam Code: CIMAPRA17-BA2-1-ENG

- Exam Name: BA2 - Fundamentals of Management Accounting (2017 SYLLABUS) (Online)

- Certification Provider: CIMA

- Latest update: Jan 06,2026

The variable overhead expenditure variance is:

- A . The over or under absorbed variable overhead

- B . The difference between the actual hours worked and the standard hours produced, multiplied by the variable overhead absorption rate

- C . The actual hours worked multiplied by the variable absorption rate

- D . The difference between the variable overheads incurred and the flexed budget allowance for variable overheads

An increase in the variable cost per unit, will cause the point at which the line plotted on a profit/volume (PV) graph intersects the horizontal axis to:

- A . Move to the left

- B . Move to the right

- C . Double

- D . Stay where it is

C Ltd produces a chemical in a single process. Information for this process last month is as follows:

(a) Opening work in progress – 10000 kg valued at £10000 for direct material and £7500 for conversion costs.

(b) Materials input – 25000 kg at £1.10 per kg.

(c) Conversion costs – £17000

(d) Output during the month – 23000 kg.

(e) There were 7500 units of closing work in progress which was complete as to materials and 30% complete as to conversion.

(f) Normal loss for the month was 10% of input and all losses have a scrap value of 80p per kg.

What was the average cost per kg of finished output during the month?

- A . £1.10

- B . £1.78

- C . £1.90

- D . £1.99

The management accountant has completed the appraisal of an investment in new office equipment.

It has now been discovered that the cost of capital used in the appraisal should have been higher.

What will be the effect on the calculated net present value (NPV) and the payback period?

- A . NPV increase; payback period increase

- B . NPV decrease; payback period decrease

- C . NPV decrease; payback period stay the same

- D . NPV decrease; payback period increase

The standard labour cost for 1 component is $15.00 (5 hours at $3 per hour). Last month, 6,000 hours were worked at a cost of $17,000 to produce 1,100 components.

The labour efficiency variance was:

- A . $1,500 Adverse

- B . $1,000 Adverse

- C . $1,000 Favourable

- D . $1,500 Favourable

Which of the following cannot be used to split costs into fixed and variable elements?

- A . Absorption costing

- B . High-low method

- C . Scattergraph

- D . Line of best fit

CORRECT TEXT

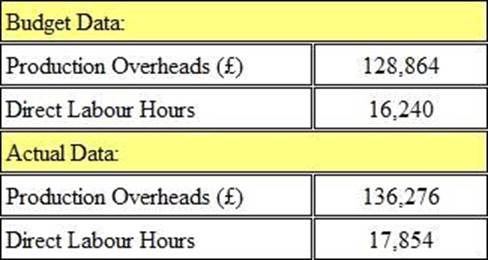

Refer to the exhibit.

The following data relates to Department A within a business unit.

The overhead absorption rate per direct labour hour for Department A is:

Give your answer to 2 decimal places.

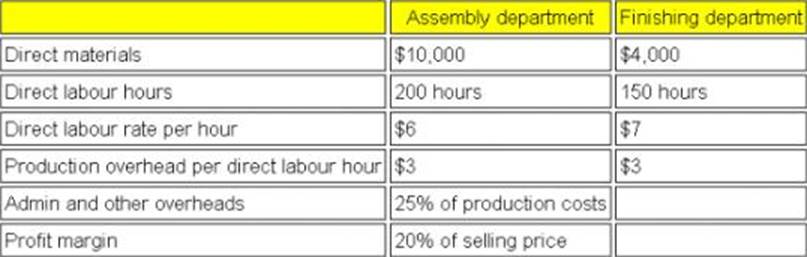

CORRECT TEXT

Refer to the exhibit.

The following information relates to Job 123:

The selling price to the customer for Job 123 is:

If the fixed costs are increased, the point at which the line plotted on a profit/volume (PV) graph cuts the horizontal axis will:

- A . Double

- B . Move to the left

- C . Stay the same

- D . Move to the right

Which one of the following is a characteristic of strategic financial information?

- A . Detailed and accurate

- B . Provided mainly to junior managers

- C . Provided daily to keep managers informed

- D . Provides information for long term decision making

Latest CIMAPRA17-BA2-1-ENG Dumps Valid Version with 392 Q&As

Latest And Valid Q&A | Instant Download | Once Fail, Full Refund