CORRECT TEXT

Refer to the exhibit.

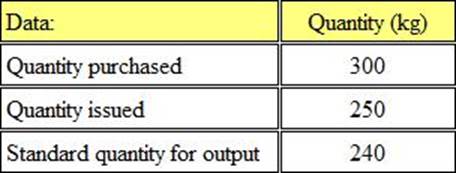

Each unit of product ‘Smitten’ uses 5 kgs of material ‘Z’.

The budgeted details for March are as follows:

It is anticipated that sales of product ‘Smitten’ in March will be 20000 units.

The amount of material ‘Z’ that needs to be purchased in March is:

A company’s cash budgetary plans show that there will be surplus cash for three months of the forthcoming year.

Which THREE of the following would be appropriate management actions in this situation?

- A . Offer a longer credit period to new customers to boost sales

- B . Purchase new non-current assets to increase efficiency

- C . Reduce the finished goods inventory to save storage costs

- D . Pay suppliers early to obtain prompt payment discounts

- E . Repay a long-term loan to reduce interest costs

- F . Invest in a short-term deposit account

Refer to the Exhibit.

PD manufactures a product in a process operation. Normal loss is 5% of input and occurs at the end of the process.

The following data is available for the month of August:

Scrapped units have no value.

There was no opening or closing work in progress for August.

What is the value of the abnormal gain in August?

- A . Nil

- B . $1,880

- C . $1,816

- D . $893

In an integrated cost and financial accounting system, the accounting entries for the payment of net wages to indirect production workers would be:

- A . Debit: Bank accountCredit: Wages control account

- B . Debit: Work in progress control accountCredit: Bank account

- C . Debit: Wages control accountCredit: Bank account

- D . Debit: Production overhead control accountCredit: Bank account

A company uses an integrated accounting system.

The accounting entries for the sale of goods on credit would bE.

- A . Debit: Receivables control accountCredit: Sales account

- B . Debit: Sales accountCredit: Finished Goods Control account

- C . Debit: Receivables control accountCredit: Cost of sales account

- D . Debit: Sales accountCredit: Receivables control account

The materials price variance will be adverse when:

- A . The actual cost of the materials is more than the standard material cost for the output produced

- B . The actual cost of the materials purchased is more than the standard cost of the materials purchased

- C . The materials usage variance is favourable

- D . The price of materials has fallen

CORRECT TEXT

CVP Limited manufactures a single product with a selling price of $25.60. Fixed costs are $122,880 per month and the product has a profit/volume ratio of 40%.

In a month when actual sales were $358,400, CVP’s margin of safety in units was

A company operates an absorption costing system. Overheads are absorbed using a pre-determined absorption rate using labour hours. In the period actual labour hours were 10,600, 400 hours below budget. Actual overheads for the period were £234,680 and there was an under-absorption of overheads of £1,480.

What was the budgeted level of overheads?

- A . £242,000

- B . £233,200

- C . £245,072

- D . £224,720

The net present value (NPV) of an investment is as follows.

NPV at 14% = $6,320

NPV at 18% = ($4,600) negative

The internal rate of return (IRR) of the investment is closest to

- A . 14.6%

- B . 16.0%

- C . 16.3%

- D . 20.3%

Refer to the Exhibit.

AM Ltd. makes and sells a single product for which the standard cost information is as follows:

✑ Budgeted production for the period is 30000 units.

✑ The actual results for the period were as follows:

What is the variable overhead expenditure variance?

- A . 13,161 adverse

- B . 13,161 favourable

- C . 13,600 adverse

- D . 13,600 favourable

An increase in the selling price per unit, will cause the point at which the line plotted on a profit/volume (PV) graph intersects the horizontal axis to:

- A . Move to the left

- B . Move to the right

- C . Double

- D . Stay where it is

A company currently allows a discount of 20% to customers who pay at the time of purchase.

If 30% of customers pay immediately, the extra sales needed in July to increase the cash receipts in that month by £6,000 are:

- A . £7500

- B . £20000

- C . £25000

- D . £30000

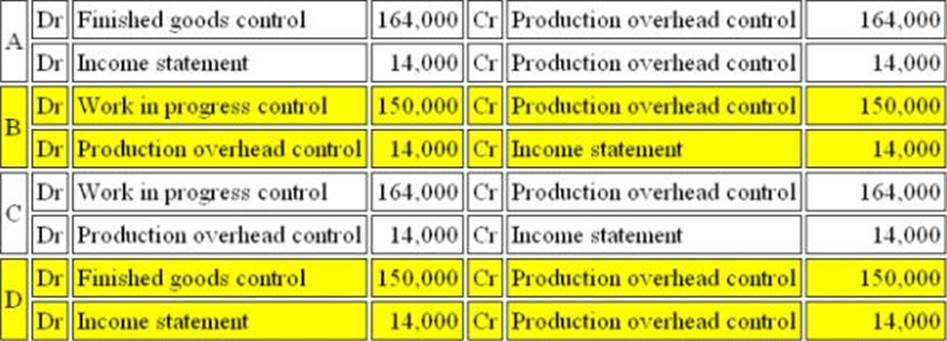

Refer to the exhibit.

WS operates an integrated accounting system.

Transactions relating to production overheads for the month of May were as follows:

Indirect Material costs were $15,000

Indirect Labour Costs were $45,000

Production overheads of $58,000 were incurred during the period.

Depreciation of factory machinery amounted to $32,000.

Overheads costs absorbed by production using a standard absorption rate was $164,000 for the period.

What are the correct entries to record the absorption of production overheads for the period?

The correct set of entries to record the absorption of production overheads for the period is:

- A . A

- B . B

- C . C

- D . D

Refer to the exhibit.

SP, a manufacturing company, uses a standard costing system.

The standard variable production overhead cost is based on the following budgeted figures for the year:

During the month of September, 5,300 actual hours were worked and 5,600 standard hours of output were produced. Total variable production overhead costs in September were $8,600.

What was the total variable production overhead variance in September?

- A . $200 adverse

- B . $650 adverse

- C . $650 favourable

- D . $200 favourable

PQR Manufacturing Ltd. has £3,000,000 of fixed costs for the forthcoming period. The company produces a single product ‘X’, which has a selling price of £75 per unit and total cost of £50.

75% of the total cost represents variable costs.

What are the break-even units?

- A . 80,000

- B . 240,000

- C . 120,000

- D . 40,000

Eton Ltd. operates a manufacturing process that produces product A.

Information for this process last month is as follows:

(a) Opening work in progress – 2,500 kg valued at £2,000 for direct material and £1,500 for labour and overheads.

(b) Materials input – 25,000 kg at £2.10 per kg.

(c) Labour – £10,000

(d) Overheads – £5,000

(e) Output during the month – 20,000 kg.

(f) There were 7,500 units of closing work in progress which was complete as to materials and 30% complete as to conversion.

(g) Normal loss for the month was 3% of input and all losses have a scrap value of £1 per kg.

What was the average cost per kg of finished output during the month?

- A . £1.73

- B . £2.72

- C . £2.78

- D . £2.80

Refer to the Exhibit.

Fabex Ltd manufactures a household detergent called "Clear".

The standard data for one of the chemicals used in production (chemical XTC) is as follows:

(a) 50 litres used per 100 litres of ‘Clear’ produced

(b) Budgeted monthly production is 1000 litres of ‘Clear’.

The closing inventory of chemical XTC for November valued at standard price was as follows:

Actual results for the period during December were as follows:

(a) 500 litres of chemical XTC was purchased for £1300.

(b) 550 litres of chemical XTC was used.

(c) 900 litres of ‘Clear’ was produced.

It is company policy to extract the material price variance at the time of purchase.

What is the total direct material price variance (to the nearest whole number)?

- A . £50 adverse

- B . £50 favourable

- C . £55 adverse

- D . £55 favourable

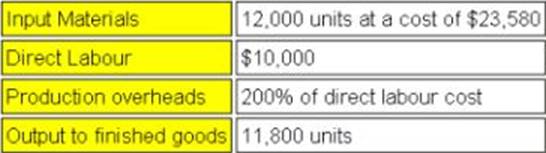

In the process account, the accounting treatment of the value of the abnormal gain is:

- A . Credit Process account Debit Abnormal Gain account

- B . Debit Process account Credit Abnormal Gain account

- C . Credit Process account Debit Normal Loss account

- D . Debit Process account Credit Normal Loss account

CORRECT TEXT

Each unit of product GM requires 4 labour hours to be produced. 25% of the units will be completed during overtime hours.

Sales of 24,000 units are planned and finished goods inventory is budgeted to rise by 2,000 units.

If the wage rate is £6 per hour and the overtime premium is 50%, what is the budgeted labour cost?

Refer to the exhibit.

![]()

T operates a process costing system. Data is available for Process A for the month of July.

Inputs for the month:

Normal losses are 15% of input and can be sold for $6 per kg. Actual output was 2,600 kg.

There is no opening or closing work in progress for the period.

What is the value of the output from the process in the month?

- A . $49,291

- B . $46,538

- C . $43,784

- D . $45,120

The variable overhead expenditure variance is:

- A . The over or under absorbed variable overhead

- B . The difference between the actual hours worked and the standard hours produced, multiplied by the variable overhead absorption rate

- C . The actual hours worked multiplied by the variable absorption rate

- D . The difference between the variable overheads incurred and the flexed budget allowance for variable overheads

An increase in the variable cost per unit, will cause the point at which the line plotted on a profit/volume (PV) graph intersects the horizontal axis to:

- A . Move to the left

- B . Move to the right

- C . Double

- D . Stay where it is

C Ltd produces a chemical in a single process. Information for this process last month is as follows:

(a) Opening work in progress – 10000 kg valued at £10000 for direct material and £7500 for conversion costs.

(b) Materials input – 25000 kg at £1.10 per kg.

(c) Conversion costs – £17000

(d) Output during the month – 23000 kg.

(e) There were 7500 units of closing work in progress which was complete as to materials and 30% complete as to conversion.

(f) Normal loss for the month was 10% of input and all losses have a scrap value of 80p per kg.

What was the average cost per kg of finished output during the month?

- A . £1.10

- B . £1.78

- C . £1.90

- D . £1.99

The management accountant has completed the appraisal of an investment in new office equipment.

It has now been discovered that the cost of capital used in the appraisal should have been higher.

What will be the effect on the calculated net present value (NPV) and the payback period?

- A . NPV increase; payback period increase

- B . NPV decrease; payback period decrease

- C . NPV decrease; payback period stay the same

- D . NPV decrease; payback period increase

The standard labour cost for 1 component is $15.00 (5 hours at $3 per hour). Last month, 6,000 hours were worked at a cost of $17,000 to produce 1,100 components.

The labour efficiency variance was:

- A . $1,500 Adverse

- B . $1,000 Adverse

- C . $1,000 Favourable

- D . $1,500 Favourable

Which of the following cannot be used to split costs into fixed and variable elements?

- A . Absorption costing

- B . High-low method

- C . Scattergraph

- D . Line of best fit

CORRECT TEXT

Refer to the exhibit.

The following data relates to Department A within a business unit.

The overhead absorption rate per direct labour hour for Department A is:

Give your answer to 2 decimal places.

CORRECT TEXT

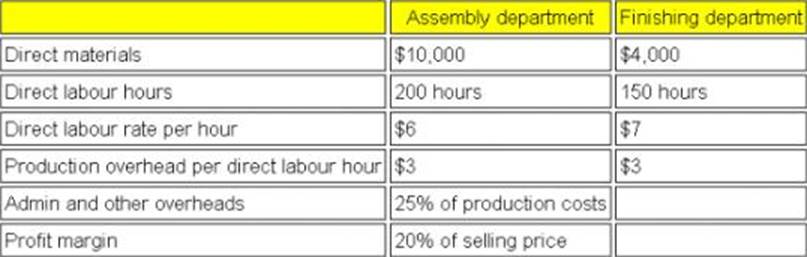

Refer to the exhibit.

The following information relates to Job 123:

The selling price to the customer for Job 123 is:

If the fixed costs are increased, the point at which the line plotted on a profit/volume (PV) graph cuts the horizontal axis will:

- A . Double

- B . Move to the left

- C . Stay the same

- D . Move to the right

Which one of the following is a characteristic of strategic financial information?

- A . Detailed and accurate

- B . Provided mainly to junior managers

- C . Provided daily to keep managers informed

- D . Provides information for long term decision making

In the process account, the accounting treatment of the value of the abnormal loss is:

- A . Credit Process account Debit Abnormal Loss account

- B . Debit Process account Credit Abnormal Loss account

- C . Credit Process account Debit Normal Loss account

- D . Debit Process account Credit Normal Loss account

A company can increase its margin of safety by which of the following independent actions?

(a) Increasing sales and production

(b) Raising the selling price per unit

(c) Raising the variable cost per unit

(d) Lowering fixed costs

- A . (a) and (b) only

- B . (a), (b) and (c) only

- C . (a), (b) and (d) only

- D . (a), (c) and (d) only

CORRECT TEXT

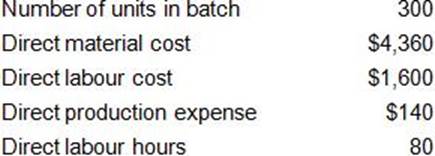

Refer to the Exhibit.

A company operates a batch costing system.

Production overhead costs are absorbed into the cost of batches using a direct labour hour rate. Other overhead costs are absorbed at a rate of 20% of total production cost. The company adds a mark-up of 10% to total cost in order to derive its selling prices.

Budgeted production overheads for the period are $44,000 and the budgeted level of activity is 8,800 direct labour hours.

The following data are available for batch number 309:

The required selling price per unit (to two decimal places) is:

Within a relevant range of output, the variable cost per unit of output will:

- A . Increase as output increases

- B . Reduce as output increases

- C . Remain constant as output increases

- D . Be impossible to tell without further information

In investment appraisal, the internal rate of return is

- A . the target rate of return for all investment proposals

- B . the rate at which a project’s cash inflows is equal to its cash outflows

- C . the rate at which the present value of a project’s cash inflows is zero

- D . the rate at which the present value of a project’s cash inflows is equal to the present value of its cash outflows

Prime cost is:

- A . Total product cost minus overheads

- B . The material cost of the product

- C . The cost of operating a cost centre

- D . All costs incurred in making a product

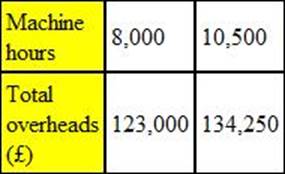

CORRECT TEXT

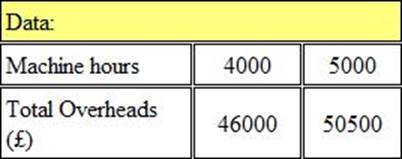

Refer to the exhibit.

The following data relates to two activity levels of a department. Overhead absorption is on the basis of machine hours.

The variable overhead rate per hour is £4.50. The amount of fixed overhead, to the nearest £000, is:

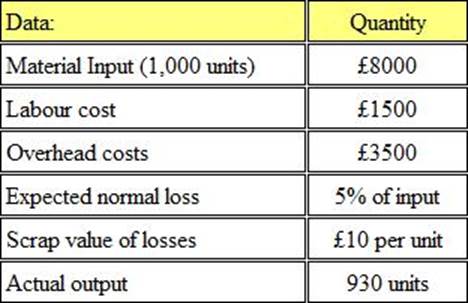

CORRECT TEXT

Refer to the exhibit.

The following information is available for a production process:

The cost per unit of good output is:

Give your answer to 2 decimal places.

Fixed costs can best be described as:

- A . Costs which are difficult to budget accurately

- B . Costs which remain constant, within a relevant range, when activity levels change

- C . Costs which never change

- D . Costs which are uncontrollable

Refer to the exhibit.

Xell Ltd uses a standard costing system and therefore values all inventory at standard cost.

During period 3 the price paid for material ‘A’ was £6 per kg less than the standard price.

The following information for material ‘A’ relates to period 3:

What was the material price variance for period 3?

- A . £6 Favourable

- B . £60 Favourable

- C . £1500 Favourable

- D . £1800 Favourable

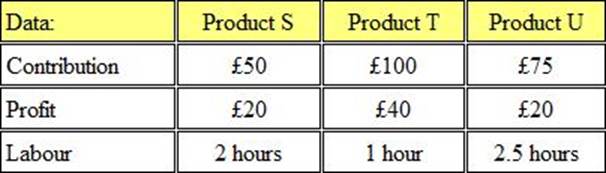

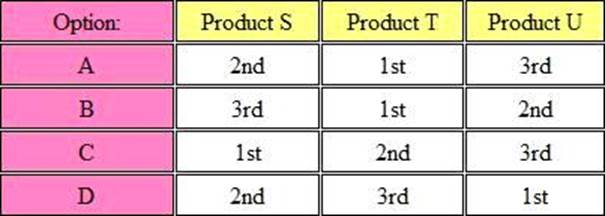

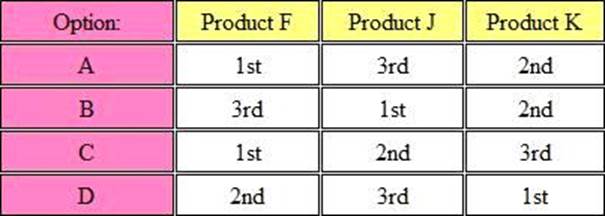

Refer to the exhibit.

C Ltd manufactures three products, which require the same type of materials.

The following contribution and profit per unit is available:

In a period in which labour hours are in short supply, which of the following options is the rank order of production?

- A . Option A

- B . Option B

- C . Option C

- D . Option D

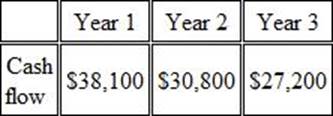

CORRECT TEXT

Refer to the Exhibit.

The following forecast cash flows relate to a proposed investment in new delivery vehicles at a total cost of $75,000.

The internal rate of return (IRR) of the proposed investment is (to two decimal places)

Within a relevant range of output, the fixed cost per unit of a product will:

- A . Increase as total output increases

- B . Remain constant as total output increases

- C . Reduce as total output increases

- D . Impossible to tell without more information

CORRECT TEXT

Refer to the Exhibit.

The following budgetary information is available for a department in a manufacturing company:

The production overhead absorption rate percentage, when the percentage on prime cost is used, is:

An overtime premium may be defined as:

- A . The rate of pay at which overtime hours are paid

- B . A premium paid to workers with special skills

- C . The additional payment made during overtime hours

- D . The total number of overtime hours worked

Which of the following categories of costs is the most relevant for decision making?

- A . Current costs

- B . Notional costs

- C . Estimated future costs

- D . Costs already incurred which are known with certainty

The decision rule to use when determining the optimal production plan if there is a scarce resource is:

- A . Maximise profit per unit

- B . Maximise profit per unit of scarce resource

- C . Maximise contribution per unit

- D . Maximise contribution per unit of scarce resource

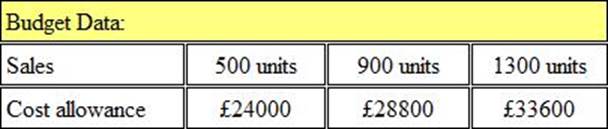

Refer to the exhibit.

Budget information for ‘Crome Ltd’ is as follows:

The budgeted cost allowance for the sale of 1000 units would be:

- A . £25,846

- B . £30,000

- C . £32,000

- D . £48,000

Which one of the following is NOT one of the five stated fundamental principles of CIMA’s code of ethics?

- A . Integrity

- B . Objectivity

- C . Punctuality

- D . Confidentiality

The accounting treatment for overheads over absorbed is to:

- A . Debit the income statement for the period

- B . Increase the cost per unit for the period

- C . Credit the income statement for the period

- D . Decrease the cost per unit for the period

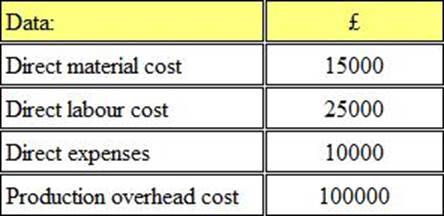

CORRECT TEXT

A company operates a full cost system of pricing. Production overheads are absorbed using a pre-determined absorption rate of £3.50 per machine hour. The direct production cost of product A is £15 per unit and it utilises 6 machine hours per unit. The mark-up for non-production costs is 10% of total production cost. The company wants to make a 25% return on sales revenue for all products.

The required selling price for Product A, to two decimal places, is:

CORRECT TEXT

A product sells for £10 per unit and has an annual break-even volume of 50,000 units. The annual fixed costs are £100,000.

The variable cost per unit is:

Give your answer to 2 decimal places.

Refer to the exhibit.

The wages analysis for the welding department of a manufacturing company is given below:

What is the direct labor cost for the welding department?

- A . $40,550

- B . $36,890

- C . $30,250

- D . $38,490

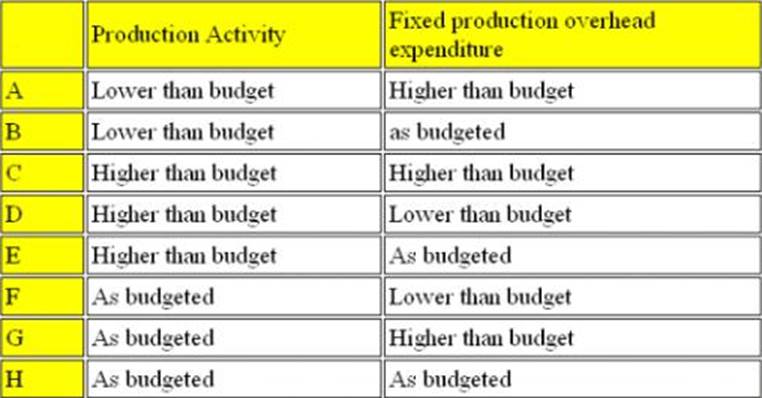

Refer to the Exhibit.

A company operates an absorption costing system. The management accounts show that fixed production overheads were over-absorbed in the period.

Which FOUR combinations could possibly have resulted in this situation?

- A . Combination A

- B . Combination B

- C . Combination C

- D . Combination D

- E . Combination E

- F . Combination F

- G . Combination G

- H . Combination H

The principal budget factor can be defined as:

- A . The factor which has the highest value in the budget

- B . The factor which limits the activities of the organisation

- C . The factor which is most likely to result in an adverse variance

- D . The factor which is least likely to change in the future

CORRECT TEXT

Apex Plc has budgeted to sell 8,000 units of A in the year. Opening inventory of A is estimated at 1,000 units and the company plans to reduce inventory levels of all products by 15%.

What will be the production budget (in units) for the year?

CORRECT TEXT

Refer to the Exhibit.

PJ Ltd has forecast that the relationship between total overheads and machine hours will be as follows:

If the budget is to be based on 4,000 machine hours, the variable overhead absorption rate will be:

*per machine hour.

Give your answer to 2 decimal places.

Which of the following industries would not use process costing?

- A . Brewing

- B . House-building

- C . Chemical

- D . Food processing

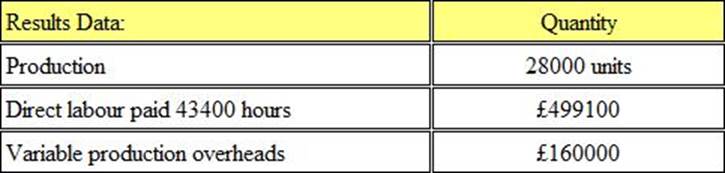

FL uses an absorption costing system. The overhead absorption rate for production overheads is $8.60 per direct labour hour.

Budgeted production overhead costs for the year were $473,000 and actual costs incurred were $468,000. 56,000 labour hours were used.

Which ONE of the following statements is correct?

- A . Overheads were under-absorbed by $5,000

- B . Overheads were over-absorbed by $8,600

- C . Overheads were under-absorbed by $8,600

- D . Overheads were over-absorbed by $13,600

A company operates an absorption costing system. Overheads are absorbed using a pre-determined absorption rate using labour hours.

Actual labour hours were 10% below budget for the period and overheads incurred were 10% above budget for the period. This would result in:

- A . An over-absorption of overheads for the period

- B . An under-absorption of overheads for the period

- C . Neither an over- or under-absorption of overheads for the period

- D . Impossible to tell from the information available

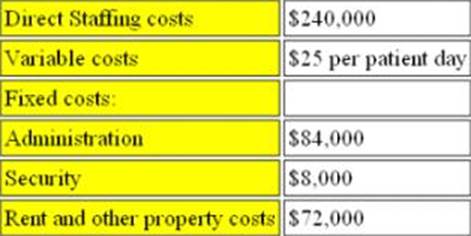

Refer to the exhibit.

X Enterprises runs a private nursing home for the elderly. The company are concerned that bed occupancy rates have been falling over the past 2 years with a consequential effect on profit.

They have drawn up a budget for next year as follows:

The nursing home currently charges $90 per patient day.

The nursing home operates at 7,500 patient days per year. In an effort to increase occupancy rates the company are proposing to reduce the current price by 10% and increase spending on advertising by $10,000 each year.

What effect will this have on the margin of safety?

- A . Reduce the margin of safety by 1,178 days

- B . Reduce the margin of safety by 622 days

- C . Increase the margin of safety by 1,178 days

- D . Increase the margin of safety by 622 days

In a manufacturing company which produces a range of products, the production manager’s salary would be classified as A.

- A . Direct labour cost

- B . Direct expense

- C . Indirect labour cost

- D . Indirect expense

The wages of a machine operator who is paid a guaranteed minimum wage plus a bonus for each unit produced would be described as A.

- A . Fixed cost

- B . Semi-variable cost

- C . Variable cost

- D . Stepped fixed cost

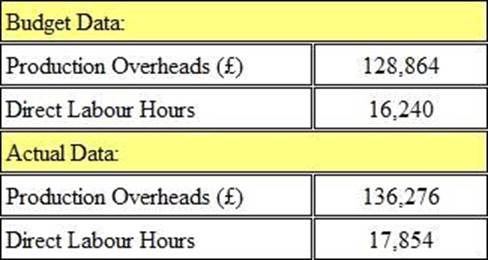

SP Limited operates an absorption costing system. It uses a predetermined overhead absorption rate based on machine hours. Budgeted factory overheads for the year were £1,080,000 but actual overhead incurred was £1,046,000. Budgeted machine hours were 120,000 and actual machine hours were 119,000.

Overheads for the period were.

- A . Under-absorbed by £25,000

- B . Under-absorbed by £9,000

- C . Over-absorbed by £25,000

- D . Over-absorbed by £9,000

The variable overhead efficiency variance is:

- A . The same as the direct labour efficiency variance

- B . The difference between the actual hours worked and the standard hours produced, multiplied by the variable overhead absorption rate

- C . The difference between the actual variable overheads incurred and those absorbed

- D . The actual hours worked multiplied by the variable overhead absorption rate

Refer to the Exhibit.

Zepher Ltd. manufactures three products, which require the same type of machine. The following fixed cost and profit per unit is available:

In a period in which machine hours are in short supply, which of the following options is the rank order of production?

Answer is:

- A . Option A

- B . Option B

- C . Option C

- D . Option D

CORRECT TEXT

A company operates a full cost system of pricing. Production overheads are absorbed using a pre-determined absorption rate of £3.50 per machine hour. The direct production cost of product A is £15 per unit and it utilises 6 machine hours per unit. The mark-up for non-production costs is 10% of total production cost. The company applies a 25% mark-up on total cost for all products.

The required selling price for Product A, to two decimal places, is:

CORRECT TEXT

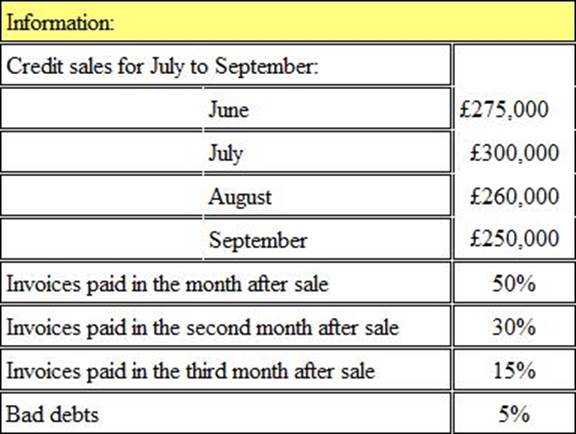

Refer to the Exhibit.

The following details have been extracted from the receivables collection records of SBC:

The amount budgeted to be received in September from credit sales is, to the nearest £000:

Each finished carton of product P contains 15 litres of liquid L. During the production process there is an unavoidable loss of 20% of the liquid input. The standard price of liquid L is $2 per litre.

The standard ingredient cost for liquid L shown on the standard cost card for one carton of product P will be

- A . $18.75

- B . $30.00

- C . $36.00

- D . $37.50

The following costs are incurred by a company which owns a five star hotel.

Which THREE of the items would normally be classified as variable costs?

- A . Advertising

- B . Food

- C . Depreciation on gym equipment

- D . Restaurant Manager’s salary

- E . Beverages

- F . Outside laundry service

Within the relevant range, a variable cost is a cost which:

- A . cannot be forecast with any degree of accuracy because of its variability.

- B . varies in total in proportion to the level of activity.

- C . varies per unit in proportion to the level of activity.

- D . varies in total in proportion to the level of inflation.

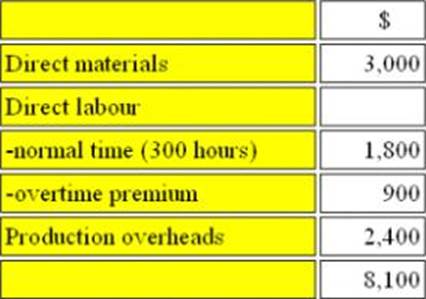

CORRECT TEXT

Refer to the exhibit.

Patchit Limited operates a job costing system. They have been asked to quote for a rush job that will require to be done in overtime hours.

It is estimated that the job will incur the following costs:

Production overheads are absorbed on a direct labour hour basis. Budgeted direct labour hours for the year were 50,000 and budgeted direct labour cost was $300,000.

If production overheads had been based on a percentage of direct labour cost, the revised production costs for the job would be:

In order to provide information that is suitable for control purposes, the budget must be:

- A . Computer generated

- B . Fixed

- C . Flexed

- D . Ideal

CORRECT TEXT

C Ltd produces a chemical in a single process. Information for this process last month is as follows:

(a) Opening work in progress – 10000 kg valued at £10000 for direct material and £7500 for conversion costs.

(b) Materials input – 25000 kg at £1.10 per kg.

(c) Conversion costs – £17000

(d) Output during the month – 23000 kg.

(e) There were 7500 units of closing work in progress which was complete as to materials and 30% complete as to conversion.

(f) Normal loss for the month was 10% of input and all losses have a scrap value of 80p per kg.

What was the value of normal loss during the month?

Which of the following best describes a step cost?

- A . A cost which remains constant until activity reaches a critical level; thereafter the cost increases to a higher level and the unit cost remains constant until the next critical activity level is reached.

- B . A cost which increases steadily until activity reaches a critical level; thereafter the cost increases to a higher level and the total cost remains constant until the next critical activity level is reached.

- C . A cost which remains constant until activity reaches a critical level; thereafter the cost increases to a higher level and the total cost remains constant until the next critical activity level is reached.

- D . A cost which increases per unit until activity reaches a critical level; thereafter the cost increases to a higher level and the unit cost remains constant until the next critical activity level is reached.

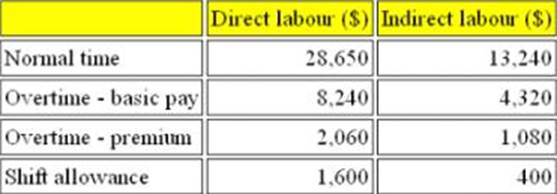

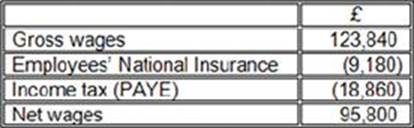

Refer to the exhibit.

DS is manufacturing company that uses an integrated accounting system.

The following payroll data is available for the month of August:

The Employers’ National Insurance for the period was $13,790.

An analysis of the wages is as follows:

Which of the following factors affect the budgeted cash flow:

(a) Funds from the issue of share capital

(b) Bank Interest on a long term loan

(c) Depreciation on fixed assets

(d) Bad debt write off

- A . Factors (a), (b), (c) and (d)

- B . Factors (a) and (b) only

- C . Factor (a) only

- D . Factors (b), (c) and (d) only

CORRECT TEXT

A company currently allows a discount of 10% to customers who pay at the time of purchase. If 20% of customers pay immediately, the extra sales needed in July to increase the cash receipts in that month by £9,000 are:

Which THREE of the following are characteristics of job costing?

- A . It is appropriate where homogeneous products are manufactured

- B . It is only appropriate in manufacturing environments

- C . Costs are traced to separately identifiable cost units

- D . It cannot be applied in a public sector or not for profit organization

- E . A separate work in progress account is maintained for each cost unit

- F . It is a specific order costing system

Refer to the exhibit.

Data for October’s budget for product Quest for the month of October are given below:

Each unit of Quest requires 6kg of raw materials. Strict quality control procedures are applied to the manufacturing process and normal rejection levels are 5% of finished units.

The raw materials purchases budget for the month of October is:

- A . 2,134,737 kg

- B . 2,136,000 kg

- C . 2,129,400 kg

- D . 2,130,600 kg

The master budget is:

- A . A consolidation of all subsidiary budgets

- B . The income statement

- C . The cash budget

- D . The budget for the principal budget factor