CFA Institute CFA Level 2 CFA Level 2 Exam Online Training

CFA Institute CFA Level 2 Online Training

The questions for CFA Level 2 were last updated at Mar 30,2026.

- Exam Code: CFA Level 2

- Exam Name: CFA Level 2 Exam

- Certification Provider: CFA Institute

- Latest update: Mar 30,2026

Martha Gillis, CFA, trades currencies for Trent, LLC. Trent is one of the largest investment firms in the world, and its foreign currency department trades more currency on a daily basis than any other firm. Gillis specializes in currencies of emerging nations.

Gillis received an invitation from the new Finance Minister of Binaria, one of the emerging nations included in Gillis’s portfolio. The minister has proposed a number of fiscal reforms that he hopes will help support Binaria’s weakening currency. He is asking currency specialists from several of the largest foreign exchange banks to visit Binaria for a conference on the planned reforms. Because of its remote location, Binaria will pay all travel expenses of the attendees, as well as lodging in government-owned facilities in the capital city. As a further inducement, attendees will also receive small bags of uncut emeralds (as emeralds are a principal export of Binaria), with an estimated market value of $500.

Gillis has approximately 25 clients that she deals with regularly, most of whom are large financial institutions interested in trading currencies. One of the services Gillis provides to these clients is a weekly summary of important trends in the emerging market currencies she follows. Gillis talks to local government officials and reads research reports prepared by local analysts, which are paid for by Trent. These inputs, along with Gillis’s interpretation, form the basis of most of Gillis’s weekly reports.

Gillis decided to attend the conference in Binaria. In anticipation of a favorable reception for the proposed reforms, Gillis purchased a long Binaria currency position in her personal account before leaving on the trip. After hearing the finance minister’s proposals in person, however, she decides that the reforms are poorly timed and likely to cause the currency to depreciate. She issues a negative recommendation upon her return. Before issuing the recommendation, she liquidates the long position in her personal account but does not take a short position.

Gillis’s supervisor, Steve Howlett, CFA, has been reviewing Gillis’s personal trading. Howlett has not seen any details of the Binaria currency trade but has found two other instances in the past year where he believes Gillis has violated Trent’s written policies regarding trading in personal accounts.

One of the currency trading strategies employed by Trent is based on interest rate parity. Trent monitors spot exchange rates, forward rates, and short-term government interest rates. On the rare occasions when the forward rates do not accurately reflect the interest differential between two countries, Trent places trades to take advantage of the riskless arbitrage opportunity. Because Trent is such a large player in the exchange markets, its transactions costs are very low, and Trent is often able to take advantage of mispricings that are too small for others to capitalize on. In describing these trading opportunities to clients, Trent suggests that "clients willing to participate in this type of arbitrage strategy are guaranteed riskless profits until the market pricing returns to equilibrium."

Trent’s arbitrage trading based on interest rate parity is successful mostly due to Trent’s large size, which provides it with an advantage relative to smaller, competing currency trading firms. Has Trent violated CFA Institute Standards of Professional Conduct with respect to its trading strategy or its guarantee of results?

- A . The trading strategy and guarantee of results arc both violations cf CFA Institute Standards.

- B . The trading strategy is legitimate and does not violate CFA Institute Standards, but the guarantee of investment return is a violation of Standards.

- C . Both the trading strategy and guarantee statement comply with CFA Institute Standards.

SIMULATION

Ota L’Abbe, a supervisor at an investment research firm, has asked one of the junior analysts, Andreas Hally, to draft a research report dealing with various accounting issues.

Excerpts from the request are as follows:

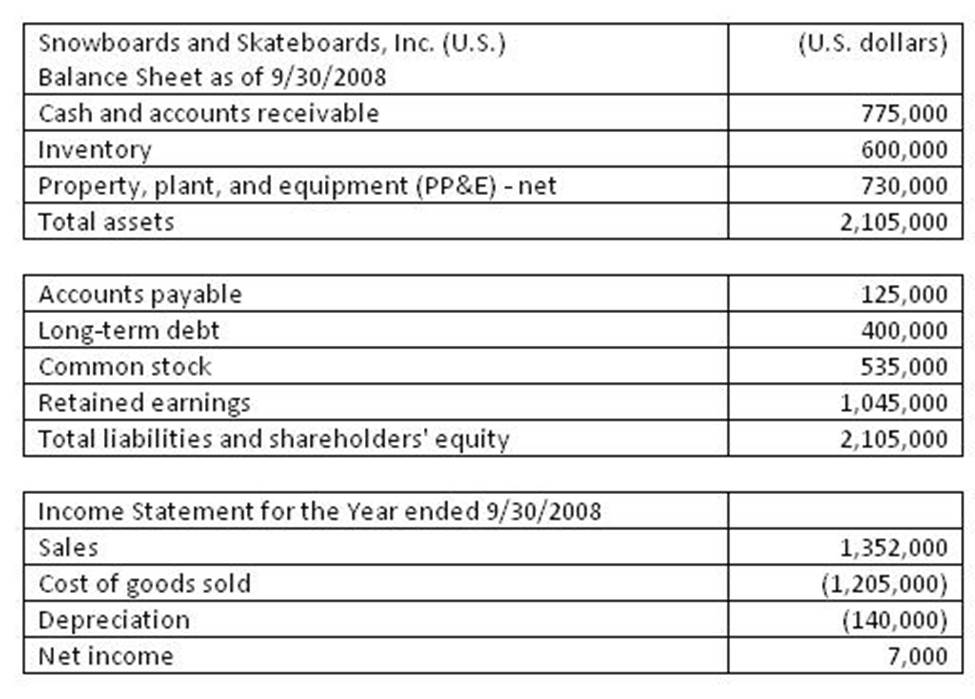

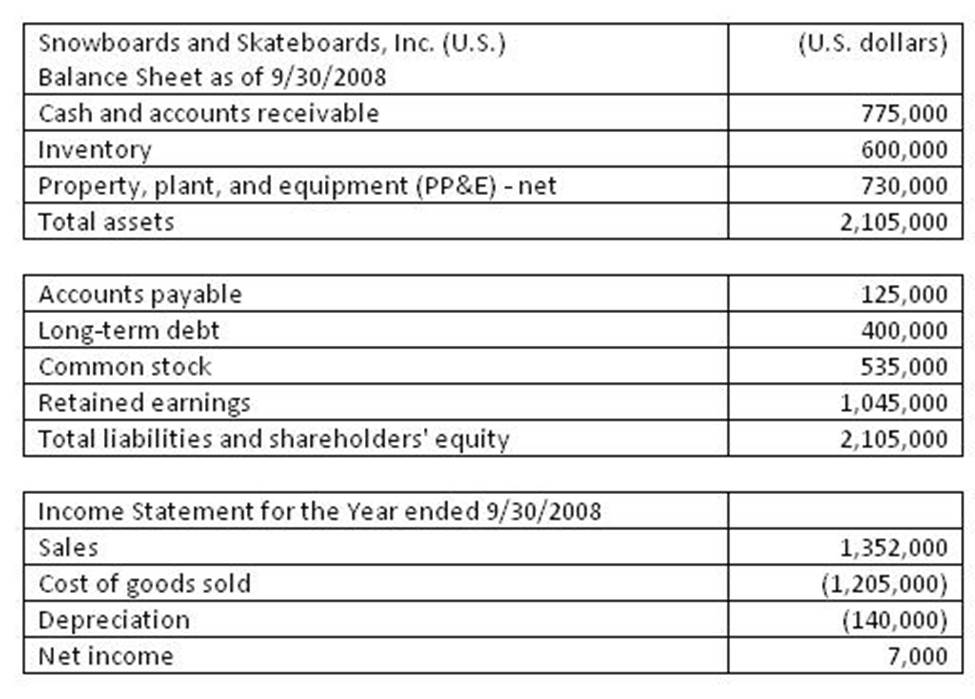

• “There’s an exciting company that we’re starting to follow these days. It’s called Snowboards and Skateboards, Inc. They are a multinational company with operations and a head office based in the resort town of Whistler in western Canada. However, they also have a significant subsidiary located in the United States."

• "Look at the subsidiary and deal with some foreign currency issues including the specific differences between the temporal and all-current methods of translation, as well as the effect on financial ratios."

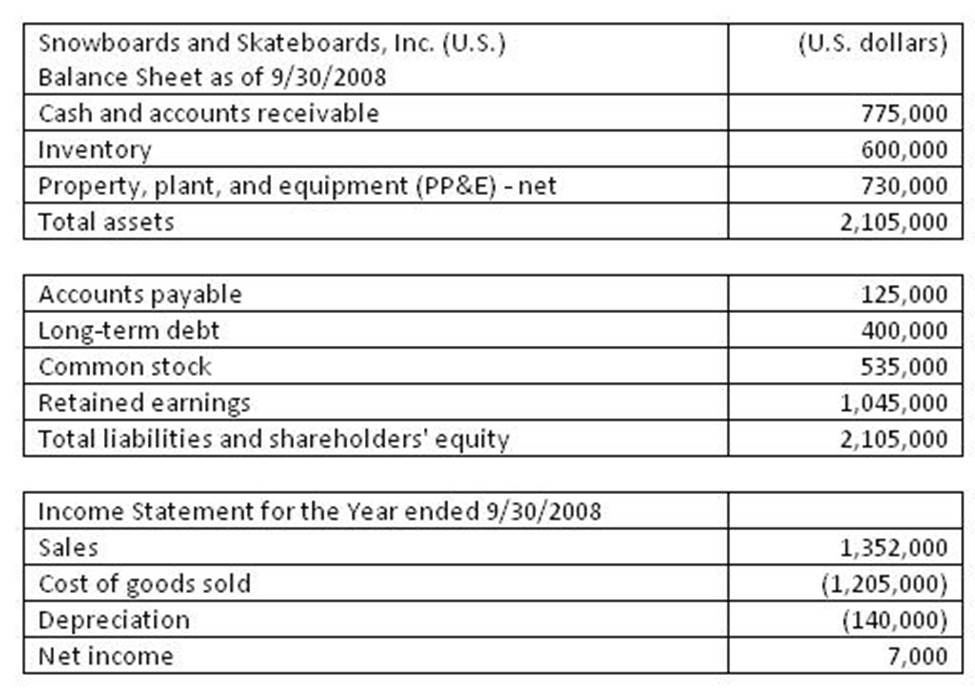

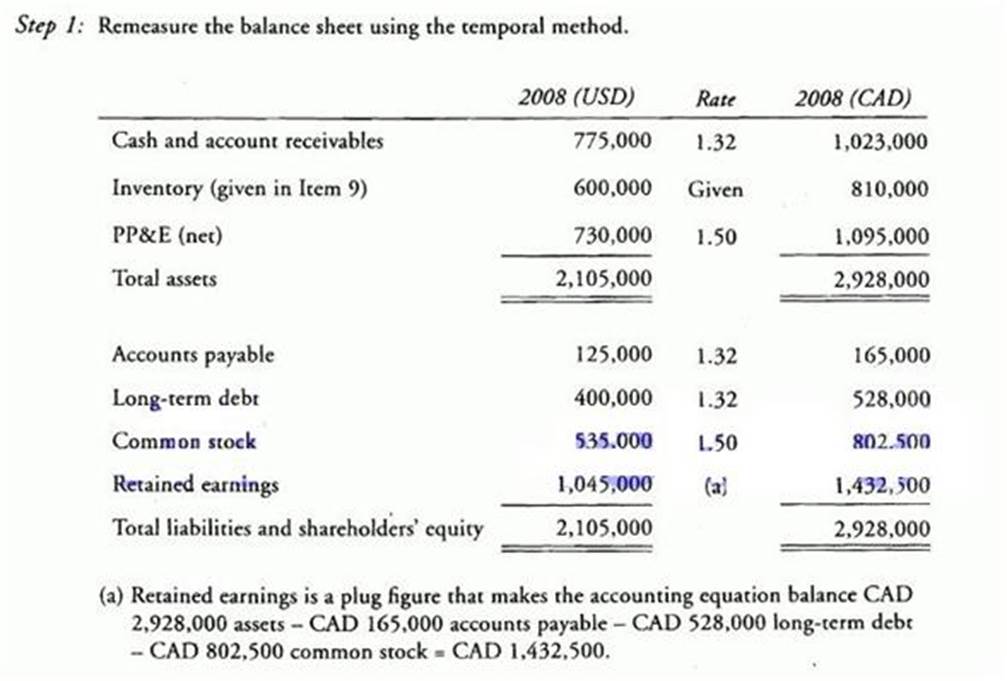

• "The attached file contains the September 30, 2008, financial statements of the U.S. subsidiary. Translate the financial statements into Canadian dollars in a manner consistent with U.S. GAAP."

The following are statements from the research report subsequently written by Hally:

Statement 1: Subsidiaries whose operations are well integrated with the parent will use the all-current method of translation.

Statement 2: Self-contained, independent subsidiaries whose operating, investing, and financing activities are primarily located in the local market will use the temporal method of translation.

Other information to be considered

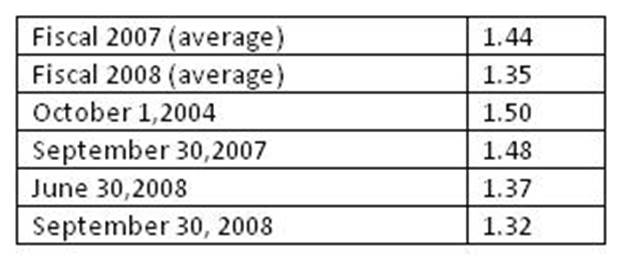

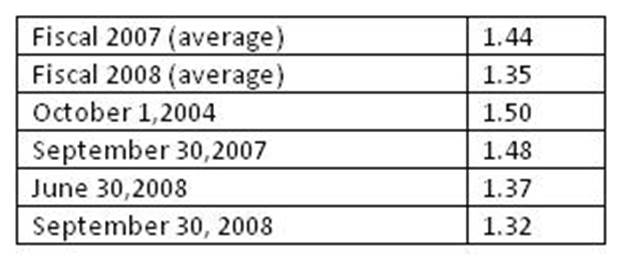

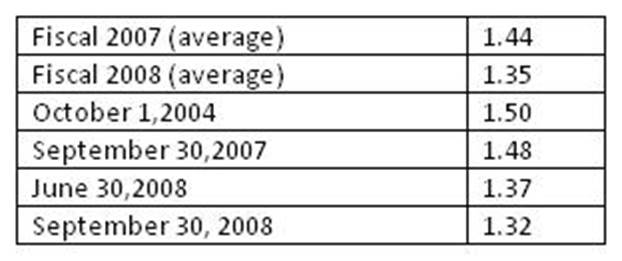

• Exchange rates (CAD/USD)

• Beginning inventory for fiscal 2008 had been purchased evenly throughout fiscal 2007. The company uses the FIFO inventory value method.

• Dividends of USD 25,000 were paid to the shareholders on June 30, 2008.

• All of the remaining inventory at the end of fiscal 2008 was purchased evenly throughout fiscal 2008.

• All of the PP&E was purchased, and all of the common equity was issued at the inception of the company on October 1, 2004. No new PP&E has been acquired, and no additional common stock has been issued since then. However, they plan to purchase new PP&E starting in fiscal 2009.

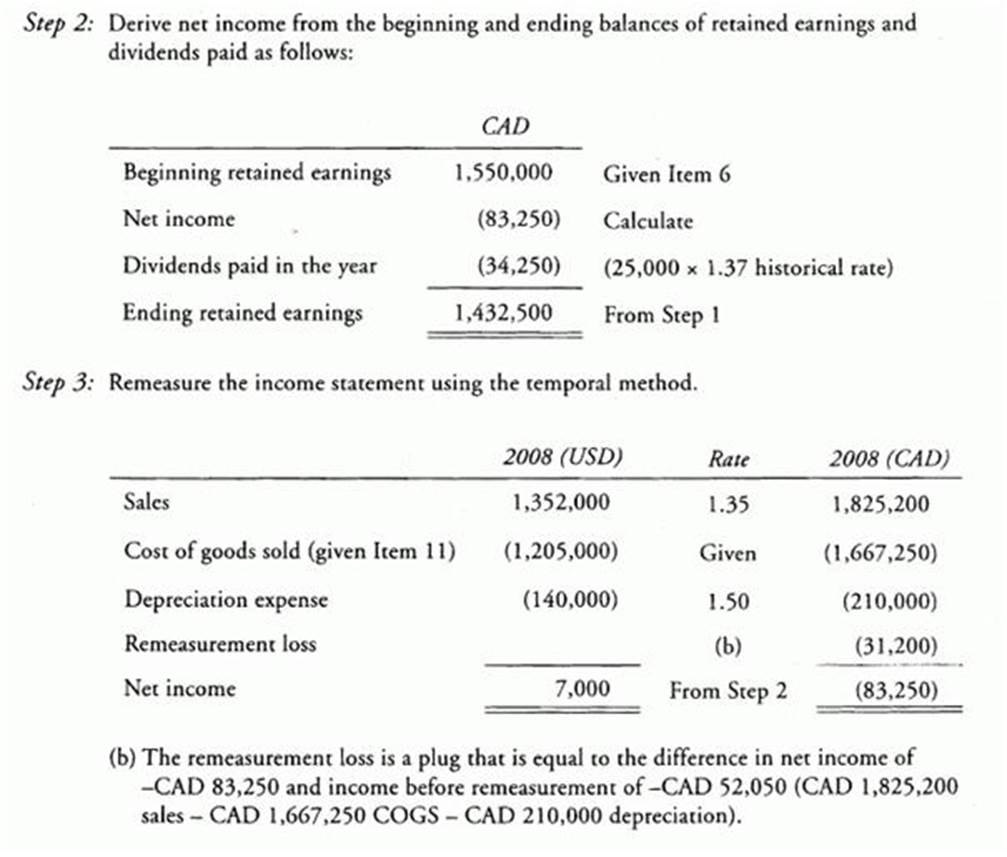

• The beginning retained earnings balance for fiscal 2008 was CAD 1,550,000.

• The accounts payable on the fiscal 2008 balance sheet were all incurred on June 30, 2008.

• The U.S. subsidiary’s operations are highly integrated with the main operations in Canada.

• The remeasured inventory for 2008 using the temporal method is CAD 810,000.

• All monetary asset and liability balances are the same as they were at the end of the 2007 fiscal year, except that long-term debt was USD 467,700.

• Costs of goods sold under the temporal method in 2008 is CAD 1,667,250.

Which of the following best describes the effect on the parent’s fiscal 2008 sales when translated to Canadian dollars? Sales, relative to what it would have been if the CAD/USD exchange rate had not changed, will be:

- A . lower because the U.S. dollar depreciated during fiscal 2008.

- B . higher because the average value of the Canadian dollar depreciated during fiscal 2008.

- C . lower because the U.S. dollar appreciated during fiscal 2008.

SIMULATION

Ota L’Abbe, a supervisor at an investment research firm, has asked one of the junior analysts, Andreas Hally, to draft a research report dealing with various accounting issues.

Excerpts from the request are as follows:

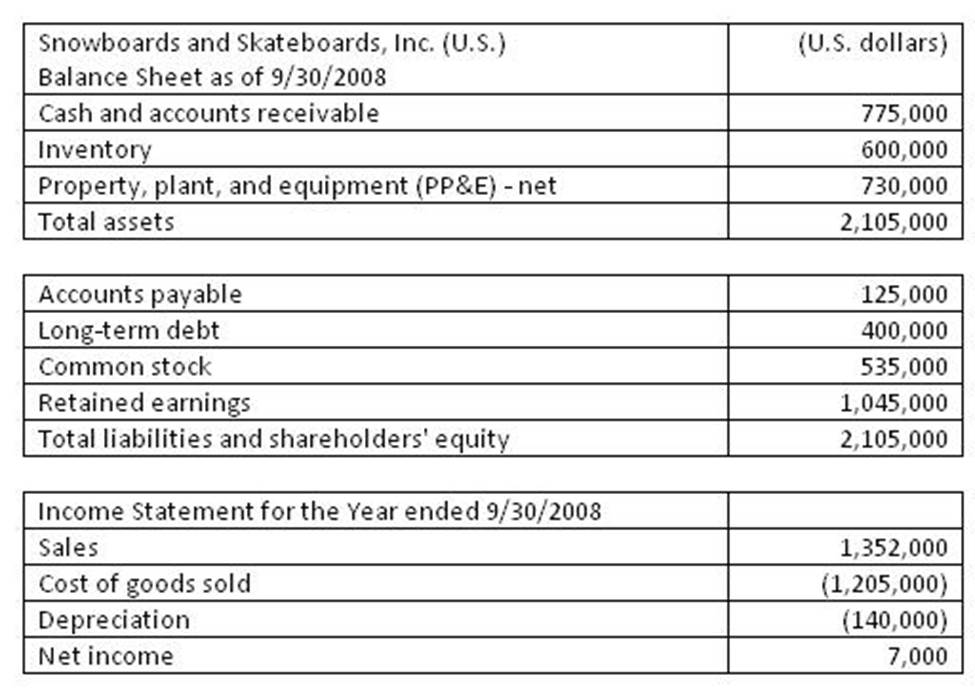

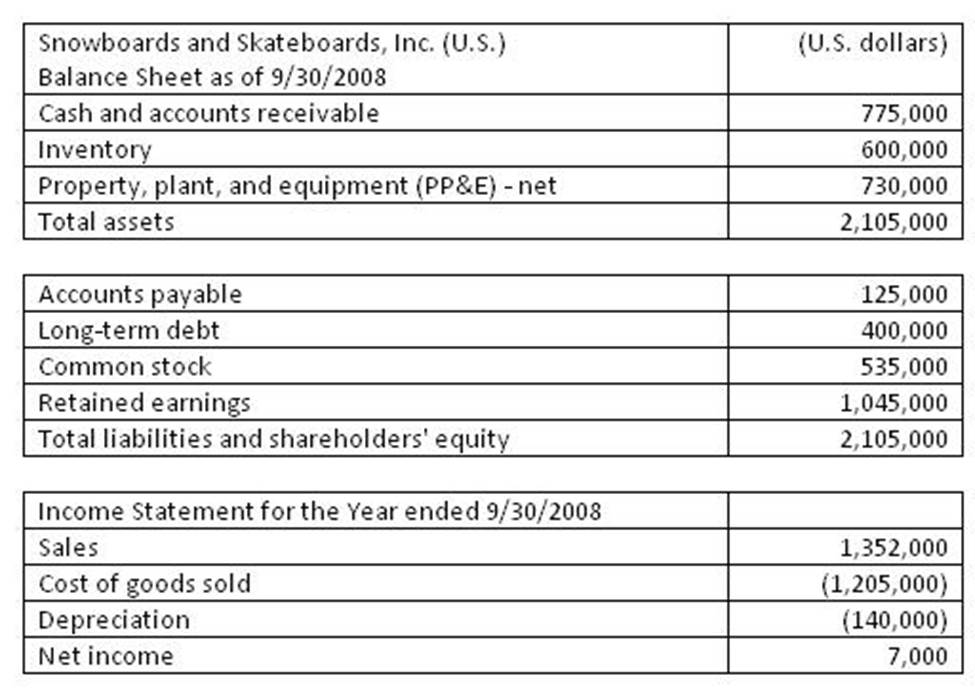

• “There’s an exciting company that we’re starting to follow these days. It’s called Snowboards and Skateboards, Inc. They are a multinational company with operations and a head office based in the resort town of Whistler in western Canada. However, they also have a significant subsidiary located in the United States."

• "Look at the subsidiary and deal with some foreign currency issues including the specific differences between the temporal and all-current methods of translation, as well as the effect on financial ratios."

• "The attached file contains the September 30, 2008, financial statements of the U.S. subsidiary. Translate the financial statements into Canadian dollars in a manner consistent with U.S. GAAP."

The following are statements from the research report subsequently written by Hally:

Statement 1: Subsidiaries whose operations are well integrated with the parent will use the all-current method of translation.

Statement 2: Self-contained, independent subsidiaries whose operating, investing, and financing activities are primarily located in the local market will use the temporal method of translation.

Other information to be considered

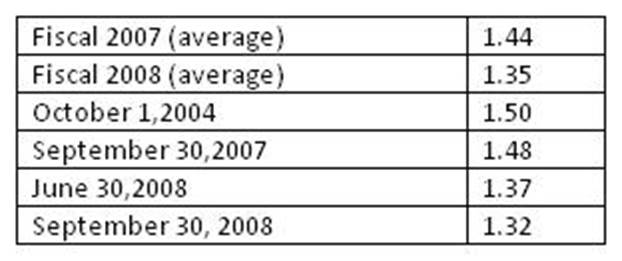

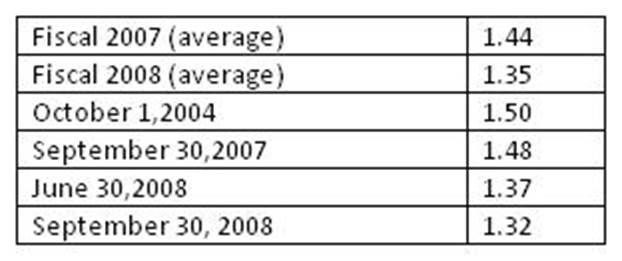

• Exchange rates (CAD/USD)

• Beginning inventory for fiscal 2008 had been purchased evenly throughout fiscal 2007. The company uses the FIFO inventory value method.

• Dividends of USD 25,000 were paid to the shareholders on June 30, 2008.

• All of the remaining inventory at the end of fiscal 2008 was purchased evenly throughout fiscal 2008.

• All of the PP&E was purchased, and all of the common equity was issued at the inception of the company on October 1, 2004. No new PP&E has been acquired, and no additional common stock has been issued since then. However, they plan to purchase new PP&E starting in fiscal 2009.

• The beginning retained earnings balance for fiscal 2008 was CAD 1,550,000.

• The accounts payable on the fiscal 2008 balance sheet were all incurred on June 30, 2008.

• The U.S. subsidiary’s operations are highly integrated with the main operations in Canada.

• The remeasured inventory for 2008 using the temporal method is CAD 810,000.

• All monetary asset and liability balances are the same as they were at the end of the 2007 fiscal year, except that long-term debt was USD 467,700.

• Costs of goods sold under the temporal method in 2008 is CAD 1,667,250.

As compared to the temporal method, which of the following financial statement elements of the parent are lower under the all-current method?

- A . Cash and accounts receivable.

- B . Depreciation expense and cost of goods sold.

- C . Common stock and dividends paid.

SIMULATION

Ota L’Abbe, a supervisor at an investment research firm, has asked one of the junior analysts, Andreas Hally, to draft a research report dealing with various accounting issues.

Excerpts from the request are as follows:

• “There’s an exciting company that we’re starting to follow these days. It’s called Snowboards and Skateboards, Inc. They are a multinational company with operations and a head office based in the resort town of Whistler in western Canada. However, they also have a significant subsidiary located in the United States."

• "Look at the subsidiary and deal with some foreign currency issues including the specific differences between the temporal and all-current methods of translation, as well as the effect on financial ratios."

• "The attached file contains the September 30, 2008, financial statements of the U.S. subsidiary. Translate the financial statements into Canadian dollars in a manner consistent with U.S. GAAP."

The following are statements from the research report subsequently written by Hally:

Statement 1: Subsidiaries whose operations are well integrated with the parent will use the all-current method of translation.

Statement 2: Self-contained, independent subsidiaries whose operating, investing, and financing activities are primarily located in the local market will use the temporal method of translation.

Other information to be considered

• Exchange rates (CAD/USD)

• Beginning inventory for fiscal 2008 had been purchased evenly throughout fiscal 2007. The company uses the FIFO inventory value method.

• Dividends of USD 25,000 were paid to the shareholders on June 30, 2008.

• All of the remaining inventory at the end of fiscal 2008 was purchased evenly throughout fiscal 2008.

• All of the PP&E was purchased, and all of the common equity was issued at the inception of the company on October 1, 2004. No new PP&E has been acquired, and no additional common stock has been issued since then. However, they plan to purchase new PP&E starting in fiscal 2009.

• The beginning retained earnings balance for fiscal 2008 was CAD 1,550,000.

• The accounts payable on the fiscal 2008 balance sheet were all incurred on June 30, 2008.

• The U.S. subsidiary’s operations are highly integrated with the main operations in Canada.

• The remeasured inventory for 2008 using the temporal method is CAD 810,000.

• All monetary asset and liability balances are the same as they were at the end of the 2007 fiscal year, except that long-term debt was USD 467,700.

• Costs of goods sold under the temporal method in 2008 is CAD 1,667,250.

Using the appropriate translation method, which of the following best describes the effect of changing exchange rates on the parent’s fiscal 2008 financial statements?

- A . An accumulated loss of CAD 242,100 is reported in the shareholders’ equity.

- B . A loss of CAD 31,200 is recognized in the income statement.

- C . A gain of CAD 27,400 is recognized in the income statement.

SIMULATION

Ota L’Abbe, a supervisor at an investment research firm, has asked one of the junior analysts, Andreas Hally, to draft a research report dealing with various accounting issues.

Excerpts from the request are as follows:

• “There’s an exciting company that we’re starting to follow these days. It’s called Snowboards and Skateboards, Inc. They are a multinational company with operations and a head office based in the resort town of Whistler in western Canada. However, they also have a significant subsidiary located in the United States."

• "Look at the subsidiary and deal with some foreign currency issues including the specific differences between the temporal and all-current methods of translation, as well as the effect on financial ratios."

• "The attached file contains the September 30, 2008, financial statements of the U.S. subsidiary. Translate the financial statements into Canadian dollars in a manner consistent with U.S. GAAP."

The following are statements from the research report subsequently written by Hally:

Statement 1: Subsidiaries whose operations are well integrated with the parent will use the all-current method of translation.

Statement 2: Self-contained, independent subsidiaries whose operating, investing, and financing activities are primarily located in the local market will use the temporal method of translation.

Other information to be considered

• Exchange rates (CAD/USD)

• Beginning inventory for fiscal 2008 had been purchased evenly throughout fiscal 2007. The company uses the FIFO inventory value method.

• Dividends of USD 25,000 were paid to the shareholders on June 30, 2008.

• All of the remaining inventory at the end of fiscal 2008 was purchased evenly throughout fiscal 2008.

• All of the PP&E was purchased, and all of the common equity was issued at the inception of the company on October 1, 2004. No new PP&E has been acquired, and no additional common stock has been issued since then. However, they plan to purchase new PP&E starting in fiscal 2009.

• The beginning retained earnings balance for fiscal 2008 was CAD 1,550,000.

• The accounts payable on the fiscal 2008 balance sheet were all incurred on June 30, 2008.

• The U.S. subsidiary’s operations are highly integrated with the main operations in Canada.

• The remeasured inventory for 2008 using the temporal method is CAD 810,000.

• All monetary asset and liability balances are the same as they were at the end of the 2007 fiscal year, except that long-term debt was USD 467,700.

• Costs of goods sold under the temporal method in 2008 is CAD 1,667,250.

As compared to the temporal method, the parent’s fixed asset turnover for fiscal 2008 using the all-current method is:

- A . higher.

- B . lower.

- C . the same.

SIMULATION

Ota L’Abbe, a supervisor at an investment research firm, has asked one of the junior analysts, Andreas Hally, to draft a research report dealing with various accounting issues.

Excerpts from the request are as follows:

• “There’s an exciting company that we’re starting to follow these days. It’s called Snowboards and Skateboards, Inc. They are a multinational company with operations and a head office based in the resort town of Whistler in western Canada. However, they also have a significant subsidiary located in the United States."

• "Look at the subsidiary and deal with some foreign currency issues including the specific differences between the temporal and all-current methods of translation, as well as the effect on financial ratios."

• "The attached file contains the September 30, 2008, financial statements of the U.S. subsidiary. Translate the financial statements into Canadian dollars in a manner consistent with U.S. GAAP."

The following are statements from the research report subsequently written by Hally:

Statement 1: Subsidiaries whose operations are well integrated with the parent will use the all-current method of translation.

Statement 2: Self-contained, independent subsidiaries whose operating, investing, and financing activities are primarily located in the local market will use the temporal method of translation.

Other information to be considered

• Exchange rates (CAD/USD)

• Beginning inventory for fiscal 2008 had been purchased evenly throughout fiscal 2007. The company uses the FIFO inventory value method.

• Dividends of USD 25,000 were paid to the shareholders on June 30, 2008.

• All of the remaining inventory at the end of fiscal 2008 was purchased evenly throughout fiscal 2008.

• All of the PP&E was purchased, and all of the common equity was issued at the inception of the company on October 1, 2004. No new PP&E has been acquired, and no additional common stock has been issued since then. However, they plan to purchase new PP&E starting in fiscal 2009.

• The beginning retained earnings balance for fiscal 2008 was CAD 1,550,000.

• The accounts payable on the fiscal 2008 balance sheet were all incurred on June 30, 2008.

• The U.S. subsidiary’s operations are highly integrated with the main operations in Canada.

• The remeasured inventory for 2008 using the temporal method is CAD 810,000.

• All monetary asset and liability balances are the same as they were at the end of the 2007 fiscal year, except that long-term debt was USD 467,700.

• Costs of goods sold under the temporal method in 2008 is CAD 1,667,250.

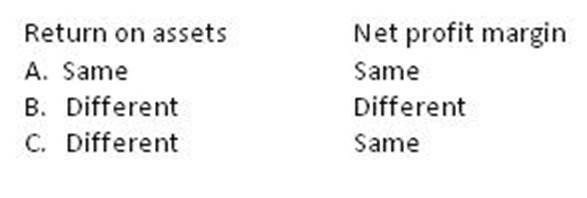

Suppose the parent uses the all-current method to translate the subsidiary for fiscal 2008. Will return on assets and net profit margin in U.S. dollars before translation be the same as, or different than, the translated Canadian dollar ratios?

Bryan Stephenson is an equity analyst and is developing a research report on Iberia Corporation at the request of his supervisor. Iberia is a conglomerate entity with significant corporate holdings in various industries. Specifically, Stephenson is interested in the effects of Iberia’s investments on its financial performance and has decided to focus on two investments: Midland Incorporated and Odessa Company.

Midland Incorporated

On December 31, 2007, Iberia purchased 5 million common shares of Midland Incorporated for 80 million. Midland has a total of 12.5 million common shares outstanding. The market value of Iberia’s investment in Midland was 89 million at the end of 2008 and 85 million at the end of 2009. For the year ended 2008, Midland reported net income of 30 million and paid dividends of 10 million. For the year ended 2009, Midland reported a loss of 5 million and paid dividends of 4 million.

During 2010, Midland sold goods to Iberia and reported 20% gross profit from the sale. Iberia sold all of the goods to a third party in 2010.

Odessa Company

On January 2, 2009, Iberia purchased 1 million common shares of Odessa Company as a long-term investment. The purchase price was 20 per share and on December 31, 2009, the market price of Odessa was 17 per share. The decline in value was considered temporary. For the year ended 2009, Odessa reported net income of 750 million and paid a dividend of 3 per share. Iberia considers its investment in Odessa as an investment in financial assets.

In addition, Iberia has a number of foreign investments, so Stephenson’s supervisor has asked him to draft a report on accounting methods and ratio analysis. The following are statements from Stephenson’s research report.

Statement 1: Under U.S. GAAP, firms are required to use proportionate consolidation to account for joint ventures.

Statement 2: In general, if the parent’s consolidated net income is positive, the equity method reports a higher net profit margin than the acquisition method.

Which of the following is the most appropriate classification of Iberia’s investment in Odessa Corporation?

- A . Held-to-maturity.

- B . Held-for-trading.

- C . Available-for-sale.

Bryan Stephenson is an equity analyst and is developing a research report on Iberia Corporation at the request of his supervisor. Iberia is a conglomerate entity with significant corporate holdings in various industries. Specifically, Stephenson is interested in the effects of Iberia’s investments on its financial performance and has decided to focus on two investments: Midland Incorporated and Odessa Company.

Midland Incorporated

On December 31, 2007, Iberia purchased 5 million common shares of Midland Incorporated for 80 million. Midland has a total of 12.5 million common shares outstanding. The market value of Iberia’s investment in Midland was 89 million at the end of 2008 and 85 million at the end of 2009. For the year ended 2008, Midland reported net income of 30 million and paid dividends of 10 million. For the year ended 2009, Midland reported a loss of 5 million and paid dividends of 4 million.

During 2010, Midland sold goods to Iberia and reported 20% gross profit from the sale. Iberia sold all of the goods to a third party in 2010.

Odessa Company

On January 2, 2009, Iberia purchased 1 million common shares of Odessa Company as a long-term investment. The purchase price was 20 per share and on December 31, 2009, the market price of Odessa was 17 per share. The decline in value was considered temporary. For the year ended 2009, Odessa reported net income of 750 million and paid a dividend of 3 per share. Iberia considers its investment in Odessa as an investment in financial assets.

In addition, Iberia has a number of foreign investments, so Stephenson’s supervisor has asked him to draft a report on accounting methods and ratio analysis. The following are statements from Stephenson’s research report.

Statement 1: Under U.S. GAAP, firms are required to use proportionate consolidation to account for joint ventures.

Statement 2: In general, if the parent’s consolidated net income is positive, the equity method reports a higher net profit margin than the acquisition method.

What amount should Iberia recognize in its 2009 income statement as a result of its investments in Midland and Odessa?

- A . 1 million profit.

- B . 2 million profit.

- C . 3 million loss.

Bryan Stephenson is an equity analyst and is developing a research report on Iberia Corporation at the request of his supervisor. Iberia is a conglomerate entity with significant corporate holdings in various industries. Specifically, Stephenson is interested in the effects of Iberia’s investments on its financial performance and has decided to focus on two investments: Midland Incorporated and Odessa Company.

Midland Incorporated

On December 31, 2007, Iberia purchased 5 million common shares of Midland Incorporated for 80 million. Midland has a total of 12.5 million common shares outstanding. The market value of Iberia’s investment in Midland was 89 million at the end of 2008 and 85 million at the end of 2009. For the year ended 2008, Midland reported net income of 30 million and paid dividends of 10 million. For the year ended 2009, Midland reported a loss of 5 million and paid dividends of 4 million.

During 2010, Midland sold goods to Iberia and reported 20% gross profit from the sale. Iberia sold all of the goods to a third party in 2010.

Odessa Company

On January 2, 2009, Iberia purchased 1 million common shares of Odessa Company as a long-term investment. The purchase price was 20 per share and on December 31, 2009, the market price of Odessa was 17 per share. The decline in value was considered temporary. For the year ended 2009, Odessa reported net income of 750 million and paid a dividend of 3 per share. Iberia considers its investment in Odessa as an investment in financial assets.

In addition, Iberia has a number of foreign investments, so Stephenson’s supervisor has asked him to draft a report on accounting methods and ratio analysis. The following are statements from Stephenson’s research report.

Statement 1: Under U.S. GAAP, firms are required to use proportionate consolidation to account for joint ventures.

Statement 2: In general, if the parent’s consolidated net income is positive, the equity method reports a higher net profit margin than the acquisition method.

What amount should Iberia report on its balance sheet at the end of 2009 as a result of its investments in Midland and Odessa?

- A . 84.4 million.

- B . 101.4 million.

- C . 102.0 million.

Bryan Stephenson is an equity analyst and is developing a research report on Iberia Corporation at the request of his supervisor. Iberia is a conglomerate entity with significant corporate holdings in various industries. Specifically, Stephenson is interested in the effects of Iberia’s investments on its financial performance and has decided to focus on two investments: Midland Incorporated and Odessa Company.

Midland Incorporated

On December 31, 2007, Iberia purchased 5 million common shares of Midland Incorporated for 80 million. Midland has a total of 12.5 million common shares outstanding. The market value of Iberia’s investment in Midland was 89 million at the end of 2008 and 85 million at the end of 2009. For the year ended 2008, Midland reported net income of 30 million and paid dividends of 10 million. For the year ended 2009, Midland reported a loss of 5 million and paid dividends of 4 million.

During 2010, Midland sold goods to Iberia and reported 20% gross profit from the sale. Iberia sold all of the goods to a third party in 2010.

Odessa Company

On January 2, 2009, Iberia purchased 1 million common shares of Odessa Company as a long-term investment. The purchase price was 20 per share and on December 31, 2009, the market price of Odessa was 17 per share. The decline in value was considered temporary. For the year ended 2009, Odessa reported net income of 750 million and paid a dividend of 3 per share. Iberia considers its investment in Odessa as an investment in financial assets.

In addition, Iberia has a number of foreign investments, so Stephenson’s supervisor has asked him to draft a report on accounting methods and ratio analysis. The following are statements from Stephenson’s research report.

Statement 1: Under U.S. GAAP, firms are required to use proportionate consolidation to account for joint ventures.

Statement 2: In general, if the parent’s consolidated net income is positive, the equity method reports a higher net profit margin than the acquisition method.

What adjustment, if any, must Iberia make to its 2010 income statement as a result of the intercompany transaction with Midland?

- A . Sales and cost of goods sold should be reduced by Iberia’s pro-rata ownership interest in the intercompany sale.

- B . Midland’s net income should be reduced by 20% of the gross profit from the intercompany sale.

- C . No adjustment is necessary.

Latest CFA Level 2 Dumps Valid Version with 713 Q&As

Latest And Valid Q&A | Instant Download | Once Fail, Full Refund