AICPA CPA-Regulation AICPA CPA Regulation Online Training

AICPA CPA-Regulation Online Training

The questions for CPA-Regulation were last updated at Jan 28,2026.

- Exam Code: CPA-Regulation

- Exam Name: AICPA CPA Regulation

- Certification Provider: AICPA

- Latest update: Jan 28,2026

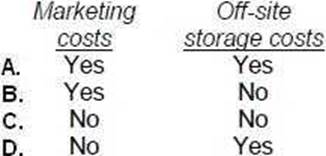

Under the uniform capitalization rules applicable to property acquired for resale, which of the following costs should be capitalized with respect to inventory if no exceptions are met?

- A . Option A

- B . Option B

- C . Option C

- D . Option D

In a tax year where the taxpayer pays qualified education expenses, interest income on the redemption of qualified U.S. Series EE Bonds may be excluded from gross income. The exclusion is subject to a modified gross income limitation and a limit of aggregate bond proceeds in excess of qualified higher education expenses.

Which of the following is (are) true?

I. The exclusion applies for education expenses incurred by the taxpayer, the taxpayer’s spouse, or any person whom the taxpayer may claim as a dependent for the year.

II. "Otherwise qualified higher education expenses" must be reduced by qualified scholarships not includible in gross income.

- A . I only.

- B . II only.

- C . Both I and II.

- D . Neither I nor II.

During 1993 Kay received interest income as follows:

On U.S. Treasury certificates $4,000

On refund of 1991 federal income tax 500

The total amount of interest subject to tax in Kay’s 1993 tax return is:

- A . $4,500

- B . $4,000

- C . $500

- D . $0

Rich is a cash basis self-employed air-conditioning repairman with 1993 gross business receipts of $20,000. Rich’s cash disbursements were as follows:

What amount should Rich report as net self-employment income?

- A . $15,100

- B . $14,900

- C . $14,100

- D . $13,900

On December 1, 1992, Michaels, a self-employed cash basis taxpayer, borrowed $100,000 to use in her business. The loan was to be repaid on November 30, 1993. Michaels paid the entire interest of $12,000 on December 1, 1992.

What amount of interest was deductible on Michaels’ 1993 income tax return?

- A . $12,000

- B . $11,000

- C . $1,000

- D . $0

On February 1, 1993, Hall learned that he was bequeathed 500 shares of common stock under his father’s will. Hall’s father had paid $2,500 for the stock in 1990. Fair market value of the stock on February 1, 1993, the date of his father’s death, was $4,000 and had increased to $5,500 six months later. The executor of the estate elected the alternate valuation date for estate tax purposes. Hall sold the stock for $4,500 on June 1, 1993, the date that the executor distributed the stock to him.

How much income should Hall include in his 1993 individual income tax return for the inheritance of the 500 shares of stock, which he received from his father’s estate?

- A . $5,500

- B . $4,000

- C . $2,500

- D . $0

John and Mary were divorced in 1991. The divorce decree provides that John pay alimony of $10,000 per year, to be reduced by 20% on their child’s 18th birthday. During 1992, John paid $7,000 directly to Mary and $3,000 to Spring College for Mary’s tuition.

What amount of these payments should be reported as income in Mary’s 1992 income tax return?

- A . $5,600

- B . $8,000

- C . $8,600

- D . $10,000

Freeman, a single individual, reported the following income in the current year:

Guaranteed payment from services rendered to a partnership $50,000

Ordinary income from a S corporation $20,000

What amount of Freeman’s income is subject to self-employment tax?

- A . $0

- B . $20,000

- C . $50,000

- D . $70,000

During 2001, Adler had the following cash receipts:

What is the total amount that must be included in gross income on Adler’s 2001 income tax return?

- A . $18,000

- B . $18,400

- C . $19,500

- D . $19,900

DAC Foundation awarded Kent $75,000 in recognition of lifelong literary achievement. Kent was not required to render future services as a condition to receive the $75,000.

What condition(s) must have been met for the award to be excluded from Kent’s gross income?

I. Kent was selected for the award by DAC without any action on Kent’s part.

II. Pursuant to Kent’s designation, DAC paid the amount of the award either to a governmental unit or to a charitable organization.

- A . I only.

- B . II only.

- C . Both I and II.

- D . Neither I nor II.

Latest CPA-Regulation Dumps Valid Version with 69 Q&As

Latest And Valid Q&A | Instant Download | Once Fail, Full Refund